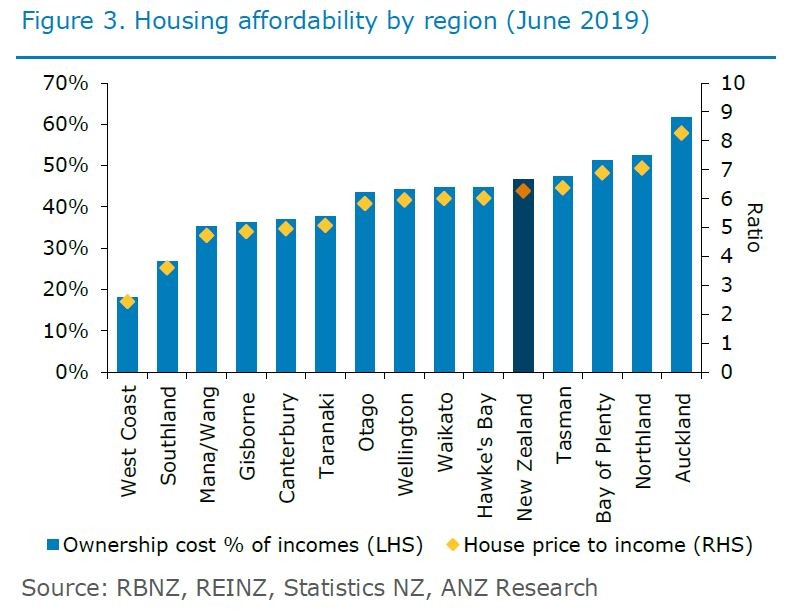

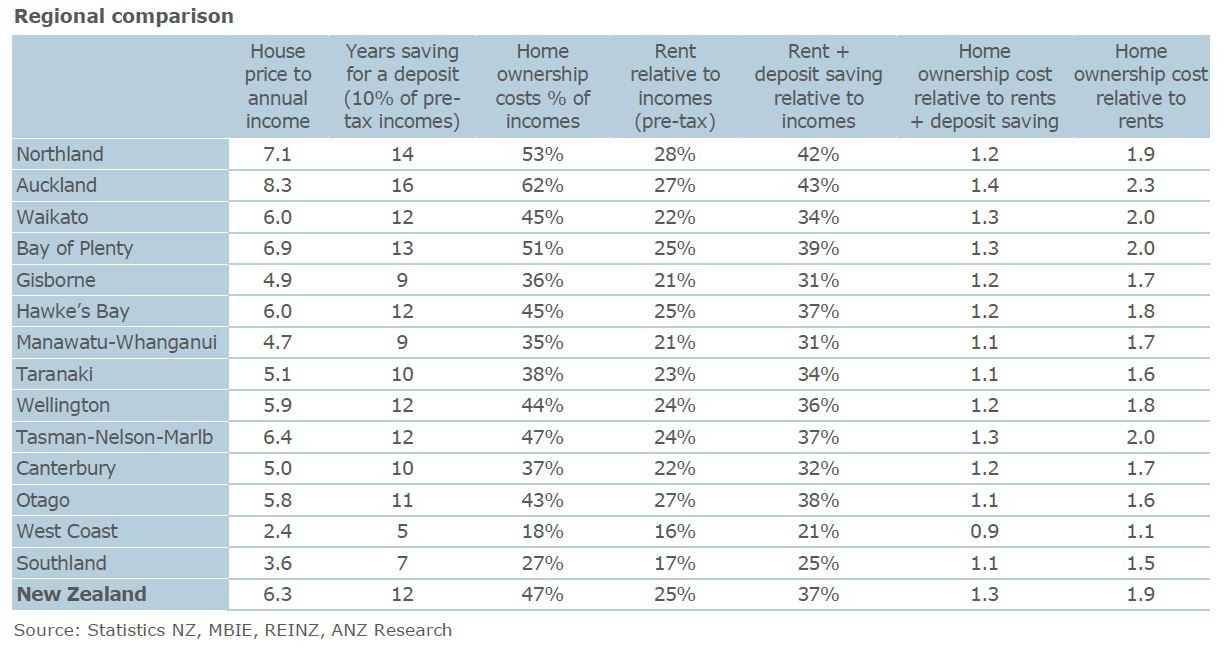

These measures are illustrative, based on median housing values and incomes. In reality, costs will depend on personal circumstances and the particular house one buys or rents. For example, most purchasers choose a lower-value property as their first step on the property ladder, but the same trends will hold.

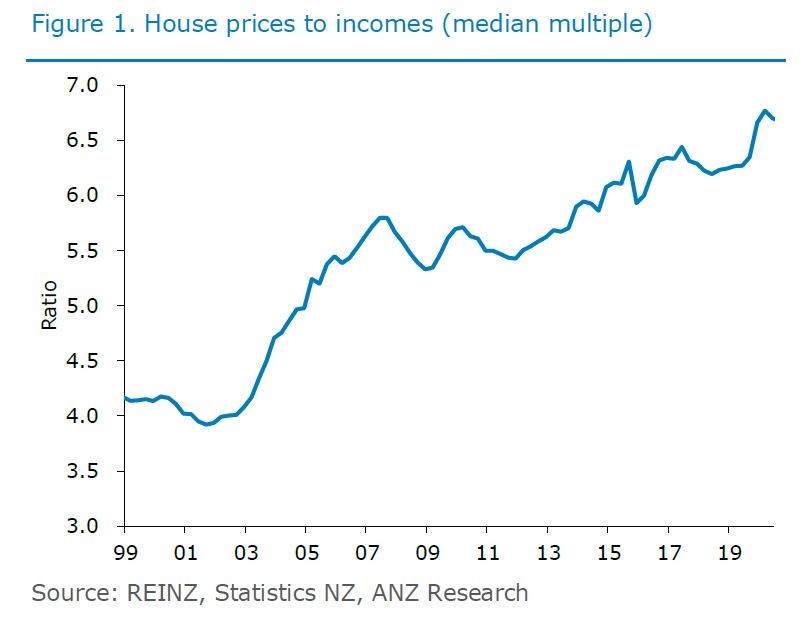

Based on these measures, houses are expensive and have become more so. Since the late 1990s, ownership costs have increased from about 35% of household incomes to around 45%, and the time taken to save for a deposit (assuming one is saving 10% of pre-tax income) has extended from 8 to almost 14 years.

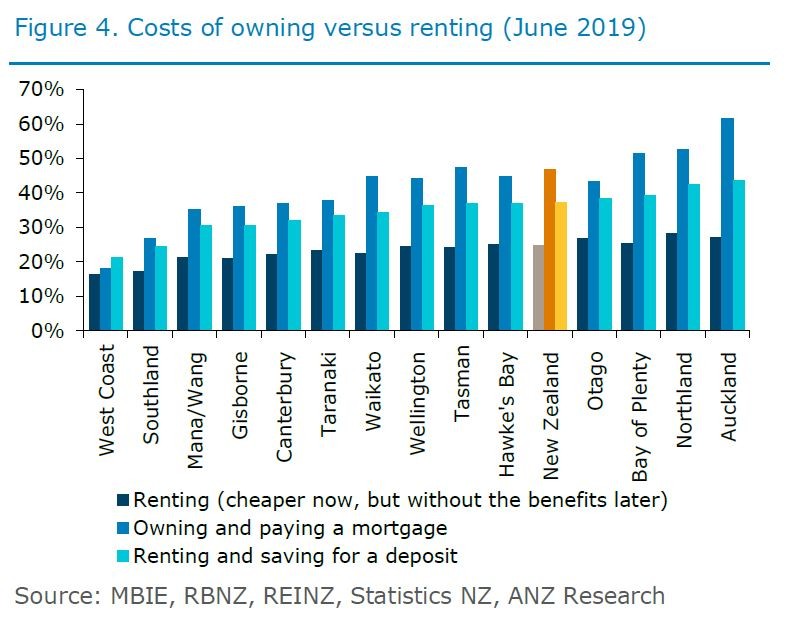

On a like-for-like basis, purchasing a new home costs about twice as much as renting. Weighing up the decision to rent or buy is very situation dependent and is contingent on personal circumstances, costs, preferences, income expectations, taxes, expectations of capital gains, and other perceived benefits.

But for those who do own their own homes, the benefits can be very substantial, including security of tenure and eventual freehold status, especially valuable in retirement. There will always be some who cannot afford to purchase a house to secure these benefits, and the cohort of people who are able and willing to do so has reduced as houses have become more expensive. The rate of home ownership has fallen from 74% in the early 90s to 65% in 2013.

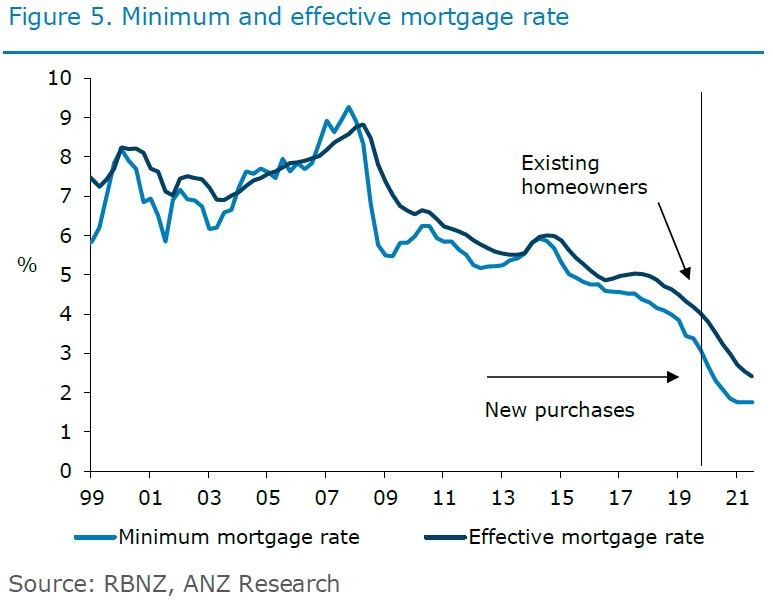

Costs of home ownership can be a significant constraint on housing affordability even with interest rates extremely low. This is because house prices, and by extension debt levels, are very high. Secular declines in mortgage rates have been more than offset by rising house prices over the past few decades.