An FLP would go hand in hand with a negative OCR and the RBNZ intends to implement one before year end. This would encourage new lending and help to ensure that retail interest rates can move even lower.

We don’t know exactly what impact these policies combined will have on mortgage rates, but the direction is clear. No, your bank won’t be paying you to borrow, but rates could get a lot cheaper.

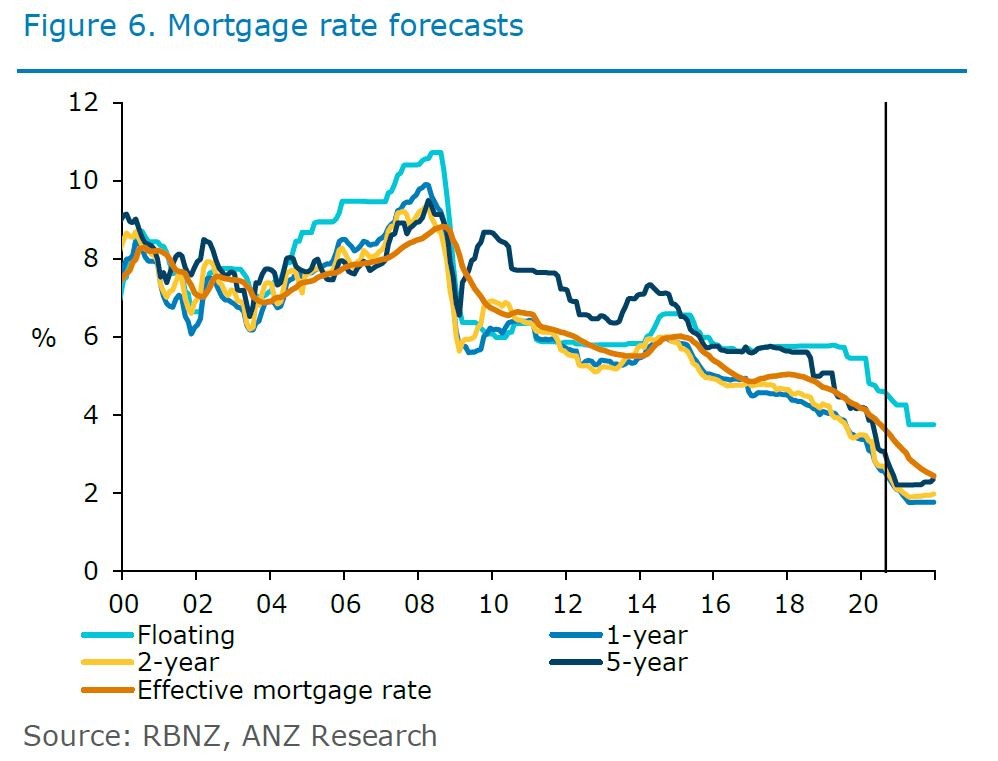

Notwithstanding considerable uncertainty, looking forward we now expect shorter-end mortgage rates to fall below 2%, with the 1-year rate expected to trough at 1.75% in April next year.

If mortgage rates continue to decline as we expect, we could see further declines in the order of 60-90bps and total falls from pre-COVID levels of up to 200bps.

Although we don’t expect the trough in mortgage rates to occur until next year, we are forecasting continued gradual declines between now and then. This assumes some compression in margins between lending and wholesale rates as the impact of QE and expectations of a negative OCR continue to percolate through.

At this stage we are only expecting one 50bp cut in the OCR in April, taking it to -0.25%. Given that the RBNZ intends to implement an FLP well before this, it is possible that the RBNZ might choose to adopt a more gradual approach to taking the OCR lower (eg pausing at 0%, or waiting until the May Monetary Policy Statement to cut).

But with economic risks skewed to the downside, and their “least regrets” approach, we also can’t rule out that the OCR might go even lower than we currently expect, in time. This would pose further downside risk to mortgage rates.

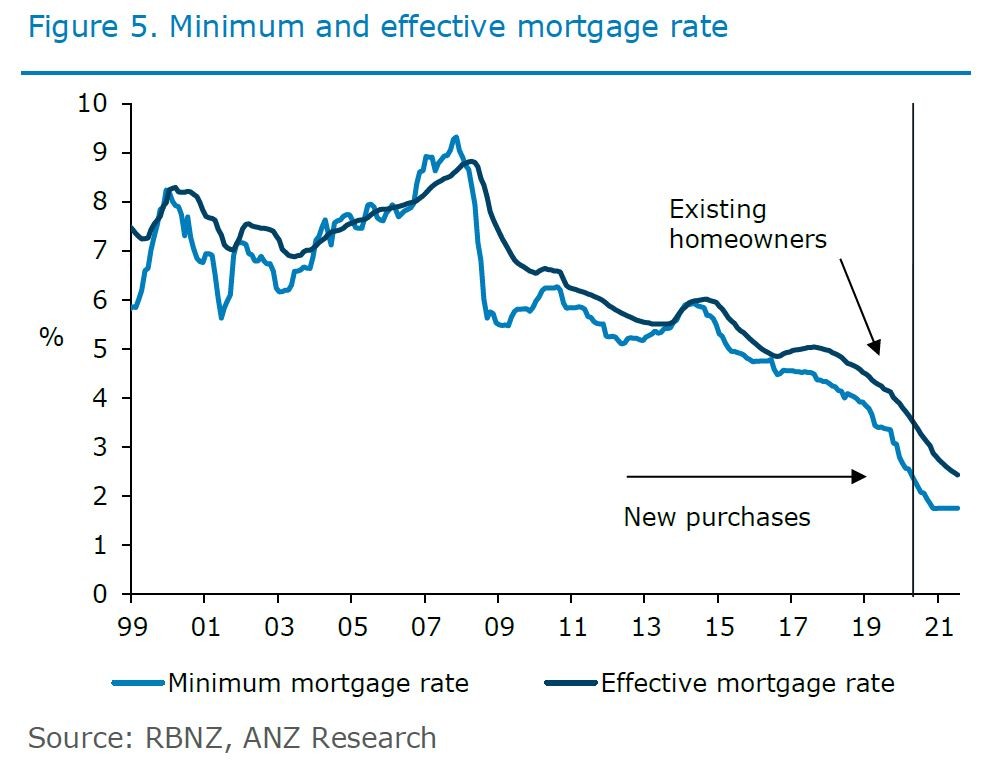

Cushion not a trampoline; risks to downside

So far, the impact of lower mortgage rates on the housing market has passed through reasonably quickly and still-lower mortgage rates will provide further support, particularly once the OCR goes negative.

But as we enter the challenging period ahead we see lower rates as a cushion, supporting the market, rather than a trampoline propelling it into the stratosphere.

All else equal, a further fall in mortgage rates as we expect might boost house prices 2-2.5%, but this is going to be competing against other dampening factors that expected to pass through to the housing market in time.

These factors are yet to become fully apparent, but that doesn’t mean the impacts have been avoided. So far, lower mortgage rates and other factors have provided a faster-acting boost.

We can’t know for sure how much of a dampening force increasing income strains and weaker net migration will be.

Forecasting the housing market is difficult at the best of times, and how a range of offsetting factors net out and impact behaviour will determine the outlook for the housing market from here, along with the underlying economic outlook, which itself is also uncertain.

It’s possible that the housing market can get through the period ahead unscathed, given the support expected from even lower rates, but at this stage we expect some wobbles will emerge, with dampening forces to weigh in time.

Risks to the economic outlook are tilted to the downside, and that’s a key reason why the RBNZ has adopted a “least regrets” approach to policy, providing monetary stimulus in a front-loaded manner.

Downside risks and the slow economic recovery ahead mean that more stimulus may be needed, even if a housing market downturn is avoided, but particularly if it isn’t.

Relative to our expectations, more stimulus might be achieved by the RBNZ taking the OCR even lower than -0.25%, a loosening of the FLP, or by expanding quantitative easing to include new assets.

But while monetary policy is working, it is not designed to cure all ills, and it does push some problems down the track rather than solve them, in terms of increasing debt. Fiscal policy needs to pivot towards supporting growth too.

Whether – and how effectively – this can be achieved will be a key factor, among others, in determining whether the RBNZ ultimately needs to do more.