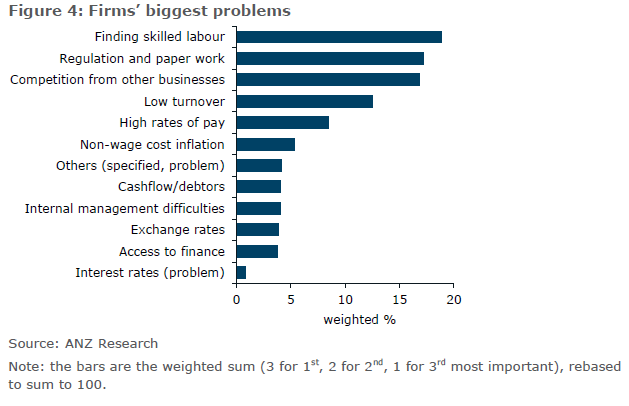

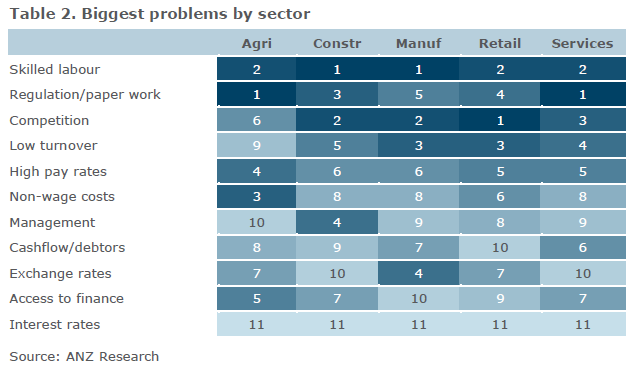

As well as what the top problems are, it’s interesting to see what isn’t a problem. Cashflow/debtors remain well down the problem list, encouragingly, as do access to finance, the exchange rate, and outside of agriculture, costs outside of wages.

And of course, it would be startling if large numbers of firms thought interest rates were a problem at present, with rates at record lows.

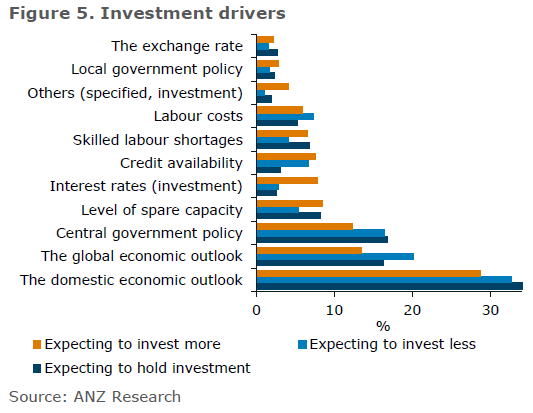

The question about investment drivers (figure 5) reveals that interest rates, while very low, aren’t a big driver of investment decisions at the moment, however.

Whether firms are intending to invest or not, the most important factors are the domestic and global economic outlooks, and central government policy.

Interest rates got an 8% weight amongst firms intending to invest more, but the domestic economic outlook was considered far more important, at 29%.

Credit availability does not seem to be much of a constraint with a weighting of just less than 8% amongst those planning on investing less (versus almost a 33% weighting on the domestic economic outlook).