NZ Business

The sustainable edge of New Zealand farmers

Businesses that have a focus on emissions stand to improve their productivity and profitability writes ANZ New Zealand Business & Agri Managing Director Lorraine Mapu.

Miles Workman

Senior Economist

ANZ Bank New Zealand Limited

Renewed Alert Level restrictions are going to weigh on activity, prolong the current bout of data volatility, push out the recovery in economic momentum, and keep the dial on monetary and fiscal stimulus turned up to eleven for even longer.

It’s worth remembering that there are three distinct prongs to this economic crisis:

So far, we’ve only really felt the pointy end of the initial lockdown. The rest (and the recessionary dynamics that will accompany them) are yet to be fully felt.

Not to mention the fact that the economy is yet to be weaned off an unprecedented amount of temporary income support (even if a little more is added in the near term).

When that happens, the deterioration in the data flow could be swift. The recent return of COVID in the community demonstrates that risks to the outlook will remain skewed to the downside for as long as the virus is a threat.

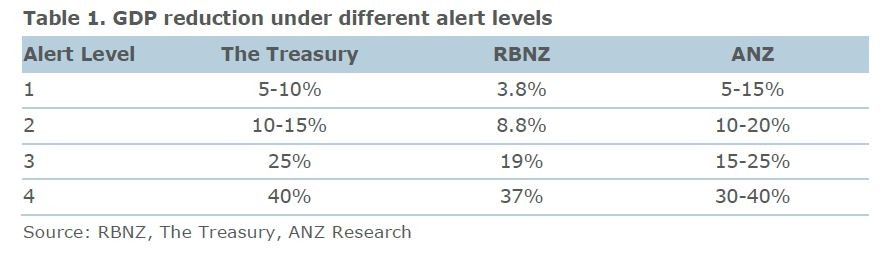

All else equal, we estimate that under Alert Level 3 the economy is able to operate at around 80% capacity and around 90% at Alert Level 2.

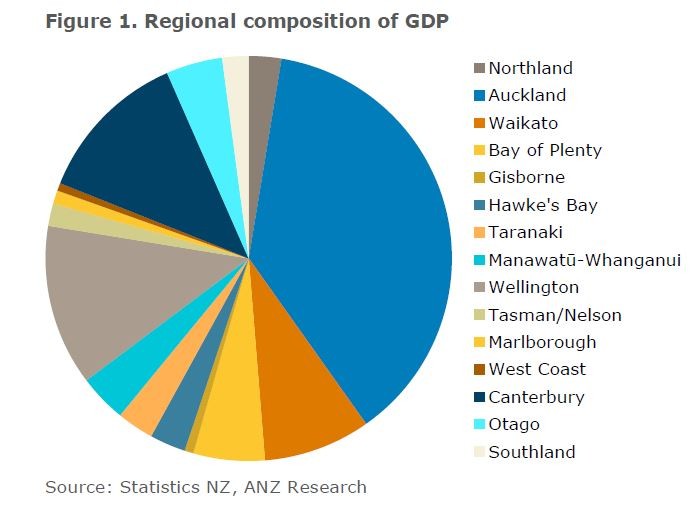

Given Auckland accounts for 38% of GDP (figure 1), we estimate that with Auckland under Alert Level 3 and the rest of NZ at Alert Level 2, nationwide activity can run at around 85% of pre-crisis levels.

For our updated forecast, we’ve assumed that this alert level status is maintained for three weeks, before the whole country returns to Alert Level 1 (where it stays until the end of 2021).

We have mitigated the risk that we phase through alert levels faster than this by assuming the impact is at the lower end of the ranges outlined in Table 1.

Auckland may also spend a couple of weeks in Level 2 as a transition phase.

However, there’s a big difference between what can happen and what will happen. And there are a number of reasons why lockdown may well hinder economic activity by more the second time around, for a given lockdown level that is.

The bottom line is that every time lockdown measures are reimposed, the underlying state of the economy will weaken further because of it, the firepower and in some cases efficacy of fiscal and monetary policy will diminish, and more stimulus will be required.

The example of Melbourne shows why hesitating for these reasons is a bad idea, but the costs are real.

The good news is that renewed lockdown measures are looking like they could be far shorter, and the paralysis of Level 4 looks set to be avoided. And despite all the gloom, there are also a few positive developments to incorporate into the outlook.

Forecasting in the current environment is riddled with challenges, the likes of which we have never experienced. Uncertainty is extreme, and typical economic relationships cannot be relied upon to hold – at least in the near term.

We need to account for a number of factors, such as pent-up demand dynamics out of lockdown, the varying impacts of a closed border at different times of the year, temporary income support measures, efficacy of the policy response more broadly, the varying impacts of the initial shock by region and industry, virus developments, and how the economic shock will broaden over time.

Further, renewed lockdown measures are likely to keep the data flow noisy for longer. And even if we pulled off a miracle and managed to forecast everything perfectly, there’s no guarantee that Stats NZ will be able to measure exactly what’s going on out there. They face significant challenges too.

But hey, let’s have a crack.

Updated GDP forecasts

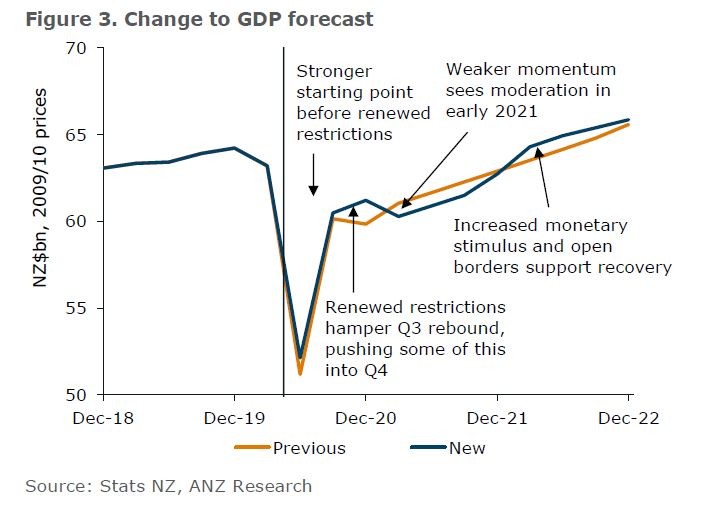

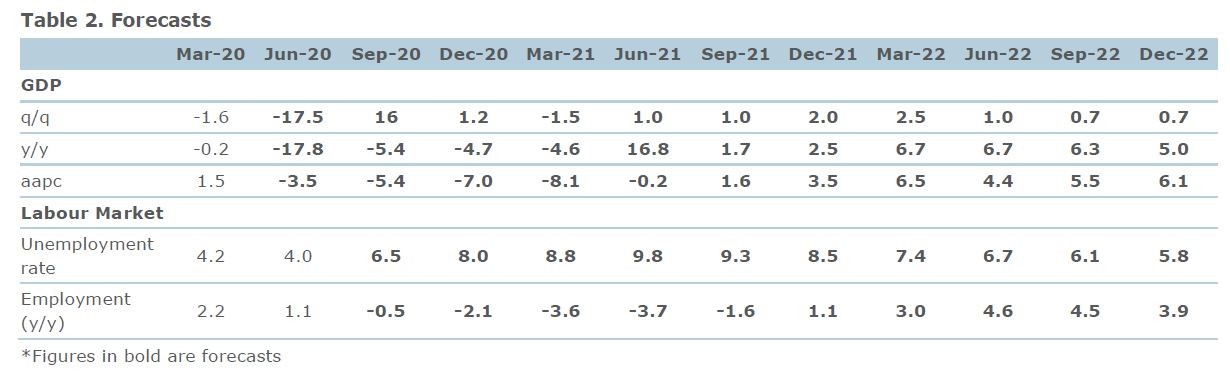

Prior to recent events, Q2 was forecast to bring a very sharp contraction in economic activity (it still is, with data out 17 September), Q3 a very sharp rebound, and Q4 the beginning of the stabilisation in quarterly GDP growth (albeit with a small quarterly fall).

Now, it looks like the Q3 rebound is going to be hampered by renewed lockdown measures, but all going well the recovery will extend into Q4 before the data begins to settle down from Q1 2021, assuming the current outbreak can be contained.

But, as noted above, we’ve had to consider a lot more than the direct impacts of lockdown. We’ve also incorporated more monetary stimulus, a solid starting point for the housing market, the vigorous bounce out of the first lockdown, and unfortunately a very weak global backdrop.

As figure 3 shows, it all nets out in a new forecast that isn’t too dissimilar to our previous view – particularly when you consider the degree of uncertainty and potential scenarios we outlined in our previous Quarterly Economic Outlook.

Conceptually, we can break down the above forecasts into three distinct components:

All of the above are non-observable factors that will cumulate into the headline GDP figures when they are released. Q2 GDP will be published on 17 September. However, we expect to get more noise than signal from these data given everything that was going on. Weaker (stronger) growth in Q2 than we expect is more likely to see us revise our Q3 forecast up (down) than convince us that the medium-term outlook has fundamentally changed.

Like GDP, there’s a lot to incorporate into the outlook for the labour market. First, there’s the starting point for the unemployment rate, which we see as containing no signal whatsoever for the underlying state of the labour market. Unemployment unexpectedly fell in Q2 on the back of both measurement challenges and a definitional quirk that meant locking down the economy also lowered the unemployment rate because people were unable to look for work during this period (and were therefore classified as being outside of the labour market). While factually correct based on the Q2 survey, the reported 4% number grossly underrepresents the many job losses that have happened and the many lives disrupted by this crisis. We certainly don’t think the Q2 read provides cause for celebration.

Broadly speaking, the labour market generally lags activity, so it’s always been our expectation that deterioration in the labour market will happen later – and wage subsidies are adding an extra delay. As noted above, there’s still a fair way to go in terms of navigating this crisis, and that’s going to keep the labour market weak for a while yet. We expect the unemployment rate to peak a little later than previously assumed, but to recover a little faster as the border reopens and more expansionary policy flows through.

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Community

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Consumer

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Media Releases

NZ Business

NZ Community

NZ Business

NZ Business

NZ Media Releases

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Sustainability

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Consumer

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Insights

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Community

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

Media

NZ Media Releases

NZ Business

NZ Business

NZ Business