NZ Media Releases

ANZ ready to support Northland customers

ANZ has support available for customers in Te Tai Tokerau impacted by power outages.

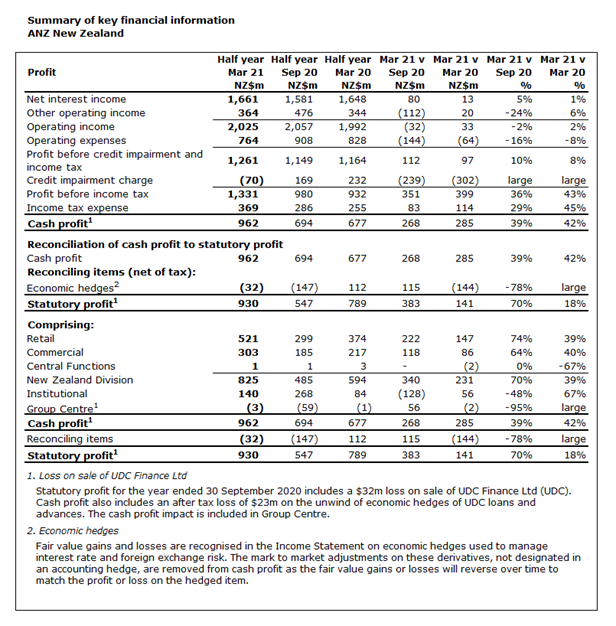

ANZ New Zealand[1] (ANZ NZ) today reported a statutory net profit after tax (NPAT) of NZ$930 million for the six months to 31 March 2021.

Cash[2] NPAT was NZ$962 million, up 42% from 31 March 2020, reflecting a strong home lending market and a significant reduction in credit impairment charges.

Expenses decreased 8% from 31 March 2020 due to lower personnel costs, a series of simplification initiatives and the divestment of UDC in September 2020. Both customer deposits and gross lending were up, 1.6% and 3.5% respectively, from 30 September 2020.

As at 31 March 2021, the ANZ Bank New Zealand Limited group remains well capitalised with a RBNZ total capital ratio of 15.9%, up from 14.4% as at 30 September 2020.

ANZ NZ Chief Executive Officer Antonia Watson said that while the full impact of Covid-19 on the New Zealand economy had yet to play out, sectors such as housing, construction and agriculture had proven resilient during the crisis.

“Across the economy, businesses have generally fared better than we expected so we’ve been able to release around 25% of the additional credit provisions we had put in place since the start of the pandemic,” Ms Watson said.

“While there’s room for optimism, we also know the impact on the economy is uneven.

“Sectors that relied on overseas visitors, such as education, hospitality and tourism, have been disproportionately affected and we’ve seen first-hand the challenges facing our customers in those industries.

“As we look ahead, a full recovery is still some way off. Economic confidence will take time to be restored as residual impacts of the pandemic are felt.

“Banks have an important role in helping New Zealanders through the recovery, and ANZ NZ is playing its part.”

ANZ NZ has been working closely with the Government and regulators to help business and retail customers manage their cash-flows and borrowings during the pandemic.

Key Points

|

· Statutory profit up 18% at NZ$930 million. · Cash profit up 42% at NZ$962 million, mainly due to lower credit impairment charges. · Revenue up 2% reflecting lending growth. · Expenses decreased 8% due to lower personnel costs, other efficiencies, and the sale of UDC in September 2020. · Credit impairment charge down $302 million from a charge of $232 million to a release of $70 million reflecting the improving economic conditions. · Total capital ratio up to 15.9%, from 14.4% as at 30 September 2020. · Customer deposits up 1.6% and gross lending up 3.5% from 30 September 2020. · KiwiSaver funds under management grew 9% to $17.9 billion from September 2020 · Acquired 12 new clearing mandates from customers, taking ANZ’s share of NZD wholesale payments to 58%. · No ordinary dividend paid to the ANZ NZ parent entity in Australia.

|

The company implemented key Government-led initiatives, such as home loan deferrals and the Business Finance Guarantee Scheme, as well as a major programme of reduced fees, charges and interest rates.

Since March 2020, ANZ NZ has offered various forms of assistance to customers including temporary deferral of principal and interest repayments, replacing principal and interest with interest only repayments, and extension of loan maturity dates. These relief packages were phased out during the six months ended 31 March 2021.

Ms Watson said the RBNZ’s use of its policy tools, including large scale asset purchases and the funding for lending programme, have kept interest rates lower and supported access to credit for borrowers.

New Zealand’s housing market defied expectations during the six-month period due to historically low interest and deposit rates, reduced loan-to-valuation ratio requirements and supply constraints.

Home lending by ANZ NZ increased $5.8 billion over the six months to 31 March 2021. In December ANZ NZ was the first bank to require a 40 per cent deposit from residential property investors as a step to bring balance to the housing market.

“It’s in everyone’s interests for residential property prices to be sustainable long term, and for home ownership to be accessible to as many people as possible,” she said.

“Another highlight was our continued development of the New Zealand Sustainable Debt Market with a number of innovative transactions including the first 30-year green bond in the New Zealand market for Auckland Council, and Mercury Limited’s inaugural green bond.

“We have also recently confirmed support for the Aotearoa Pledge, an initiative aimed at increasing the supply of affordable housing in partnership with Community Finance.”

A table of key financial information follows:

[1] ANZ New Zealand represents all of ANZ’s operations in New Zealand (NZ Geography), including ANZ Bank New Zealand Limited, its parent company ANZ Holdings (New Zealand) Limited and the New Zealand branch of ANZ.

[2] Statutory profit has been adjusted to exclude non-core items to arrive at cash profit, the result for the ongoing business activities of ANZ New Zealand. Refer to Summary of key financial information for details of reconciling items between cash profit and statutory profit.

For media enquiries contact Kristy Martin 021531402

Approved for distribution by ANZ’s Continuous Disclosure Committee

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Business

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Community

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

New Zealand

NZ Media Releases

NZ Media Releases

New Zealand

New Zealand

NZ Consumer

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

Media

NZ Consumer

Media

Media

Media

NZ Media Releases

Media

Media

NZ Media Releases

Media

NZ Community