NZ Media Releases

Nagaja Sanatkumar to be appointed to the ANZ New Zealand Board

Nagaja Sanatkumar to join the ANZ NZ Board

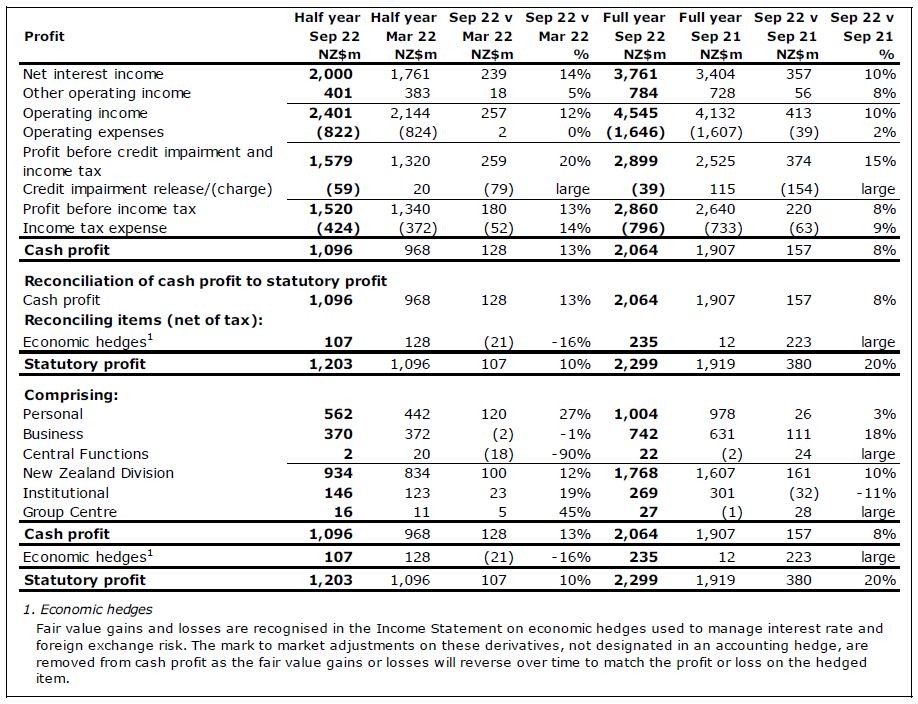

ANZ New Zealand[1] (ANZ NZ) today reported a cash[2] net profit after tax (NPAT) for the 12 months to 30 September 2022 of $2,064 million, 8% up on the 2021 financial year. Statutory NPAT, which includes gains and losses from economic hedges, was $2,299 million, a 20% increase.

ANZ Bank New Zealand Ltd (ANZ Bank NZ) Chief Executive Antonia Watson said the 8% increase in profit was a result of a combination of pent-up economic activity post the pandemic and a buoyant housing market.

“Coming into the 2021-2022 financial year we didn’t anticipate the New Zealand economy would hold up as well as it has,” Ms Watson said.

“While inflation and supply chain problems, particularly for importers and exporters, were an issue for many customers throughout the year the desire to get back to some kind of normal kept consumer spending up.

“While the housing market has quietened significantly in recent months, following four Official Cash Rate (OCR) rises since May, it was strong for most of the financial year.”

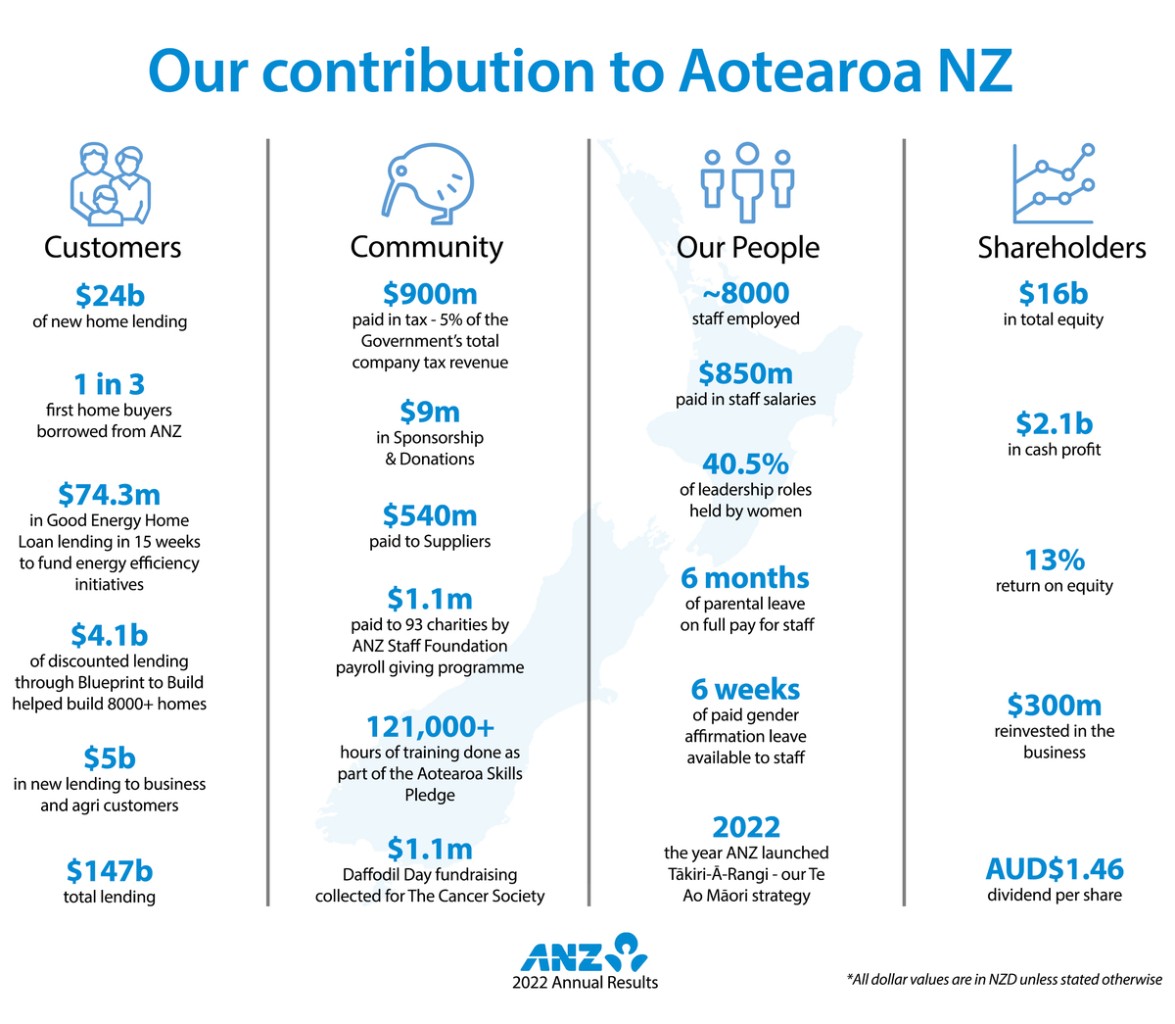

Home lending increased $5.3 billion to $104 billion over the 12 months to 30 September 2022.

Business and Institutional customers continued to manage well despite many facing challenges throughout the year, including cost inflation, supply chain difficulties, and finding staff. Non-housing lending to Business and Institutional customers — including agri — remained muted, increasing by $700 million.

The Reserve Bank of New Zealand’s (RBNZ) new capital rules equate to an increase in minimum regulatory capital required of $2.2 billion over the course of the year [3], and will require ongoing regulatory capital uplift until 2028.

“Banks are a reflection of the economies they operate in, and New Zealand has been far more resilient than expected,” Ms Watson said.

“Many of our customers have taken the opportunity to pay down debt and increase their savings. This caution is wise given the dark clouds on the horizon.

“Inflation is stubbornly high and that will mean higher costs of living and higher interest rates for longer. Global growth and geopolitical issues outside New Zealand’s control could also severely impact the country in 2023.

“The uncertain environment means New Zealanders need to be cautious.”

That was the main reason for ANZ NZ increasing its credit impairment provisions to $751m, with a $39 million charge recognised for FY22.

She said ANZ NZ had in recent months stood up a team to closely monitor customers for signs they might be concerned about managing their finances or coming under financial pressure as interest rates rise and the economy slows. It had also bolstered the bank’s Customer Financial Wellbeing team and was proactively reaching out to those who showed signs of needing reassurance and support.

“At the moment, the vast majority of customers are in a sound financial position but we know that many will roll off fixed home loans onto higher rates over the coming year. When that happens some will be under financial pressure.”

She said it wasn’t in anyone’s interests for people to get into financial stress.

“That’s why we’re keen to talk with customers sooner rather than later if there are any signs of problems to see if, for example, we can structure their finances differently to relieve some pressure.”

She said ANZ had been in the country in one form or another since 1840 and was committed to supporting New Zealanders through any tough times ahead.

“We’re in a strong position to support our customers through times of economic uncertainty and to help build future prosperity and security for Aotearoa.”

During the year ANZ NZ largely completed the delivery of the RBNZ’s new Outsourcing Policy (BS11).

The five year project came at considerable cost and requires ANZ Bank NZ to operate independently of ANZ Group systems and processes in the highly unlikely event of abrupt loss of service from ANZ Group.

All comparisons are against the prior comparable period and on a cash basis unless noted otherwise

A table of key financial information follows:

[1] ANZ New Zealand represents all of ANZ’s operations in New Zealand (NZ Geography), including ANZ Bank New Zealand Limited, its parent company ANZ Holdings (New Zealand) Limited and the New Zealand branch of ANZ.

[2] Statutory profit has been adjusted to exclude non-core items to arrive at cash profit, the result for the ongoing business activities of ANZ New Zealand. Refer to Summary of key financial information for details of reconciling items between cash profit and statutory profit.

[3] ANZ Bank NZ Ltd group increased its total regulatory capital by $1.3 billion during FY22, with the remainder having been accumulated in prior periods.

For media enquiries contact Briar McCormack, Senior Manager External Communications +64 21 280 1173

Approved for distribution by ANZ’s Continuous Disclosure Committee.

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Business

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Community

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

New Zealand

NZ Media Releases

NZ Media Releases

New Zealand

New Zealand

NZ Consumer

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

Media

NZ Consumer

Media

Media

Media

NZ Media Releases

Media

Media

NZ Media Releases

Media

NZ Community