NZ Media Releases

Nagaja Sanatkumar to be appointed to the ANZ New Zealand Board

Nagaja Sanatkumar to join the ANZ NZ Board

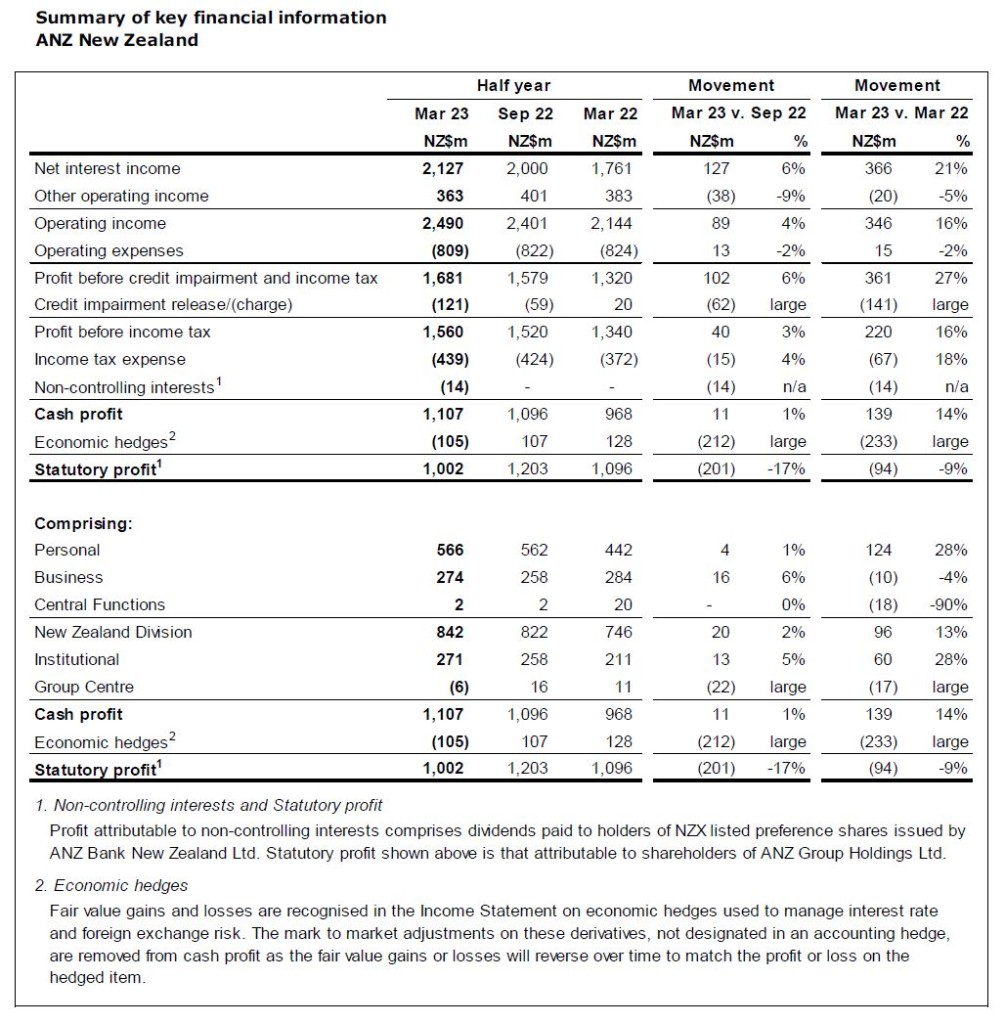

ANZ New Zealand[1] (ANZ NZ) today reported a cash net profit after tax (NPAT) of $1,107 million for the six months to 31 March 2023, a 1% increase on the six months to 30 September 2022.

Statutory NPAT[2], which includes gains and losses from economic hedges, was $1,002 million, decreasing by 17% over the same period.

All comparisons are against the six months ended 30 September 2022

ANZ Bank New Zealand CEO Antonia Watson said: “This was a good result where all parts of our business performed well and one that prepares us for the uncertain economic environment ahead.

“Our team achieved a great deal this half, including the completion of the single largest regulatory project in the history of the broader ANZ Group. Known as BS11[3], it enables us to operate independently of ANZ Group systems and processes in the unlikely event of an abrupt loss of service.

“The New Zealand economy has remained remarkably resilient, however the impact of a softening housing market, stubbornly high inflation and the impact of a rising official cash rate is starting to have a material impact on businesses and households.

“While a rising interest rate environment contributed to the result, this was offset by intense competition in home lending, which we expect to remain a feature of the market for some time into the future.

“I acknowledge this is a large profit number, however it needs to be put into the context of the size of our business and the role banks like ANZ NZ play in supporting economic activity in New Zealand, particularly during periods of uncertainty.

“The actual profitability of ANZ NZ, which measures our returns versus the amount of capital committed by shareholders, is middle of the pack when compared to large companies listed on the New Zealand stock exchange[4],” said Ms Watson.

Ms Watson also acknowledged the difficult circumstances facing New Zealanders across the country with many dealing with rising cost-of-living and recent natural disasters that have devastated large parts of the country.

“With the flooding in Auckland in January and Cyclone Gabrielle in February, this has been a tough six months for many New Zealanders. As the country’s largest bank, we are acutely aware of the role we play in supporting customers through tough times and have a team dedicated to working directly with impacted customers and communities,” Ms Watson said.

ANZ NZ has provided support for customers impacted by the floods and Cyclone Gabrielle with emergency access to over $11 million of interest free funds and has waived around $1.3 million in fees.

ANZ NZ also pledged $3 million to support communities impacted by the cyclone.

“We’ve been working with partner organisations and have made direct donations to The Red Cross Disaster Relief Fund, iwi and primary sector groups to support the incredible work they are doing with community and whānau on the ground,” she added.

Ms Watson said while the recent drop in annual inflation was encouraging, it remained at record levels with the potential for more pressure due to the impact of the recent natural disasters.

“We’re closely monitoring how our customers are managing, particularly as people come off lower fixed-rate loans. We have a team proactively contacting customers to make sure they’re aware of their options to manage repayments and provide support for those who need it.

“The reality is the Reserve Bank has been increasing the official cash rate as a necessary tool to bring down inflation, which left unchecked, will impact people’s savings, and push up cost-of-living to unsustainable levels.

“Fortunately, many of our customers took the opportunity to pay down debt while interest rates were low, and a third are ahead on their home loans by six months or more. Customers are also benefiting from term-deposit rates being around five times higher for popular terms than they were before rates began rising.”

“From talking to business customers across the country, confidence remains very subdued as high interest rates and escalating costs impact business profitability against a backdrop of weakening demand.

“Given the ongoing uncertain environment, we need to remain cautious, which is reflected in the increase in credit provisions.”

ANZ NZ recognised a credit impairment charge of $121 million, and total credit impairment provisions increased to $860 million.

Ms Watson said the Reserve Bank of New Zealand’s (RBNZ) new capital rules equate to an increase in minimum regulatory capital required of $3.3 billion by 1 July 2023 and will require ongoing regulatory capital uplift until 2028.

“Recent events in global banking also remind us of the importance of strong, safe, and well capitalised banks. Fortunately, ANZ NZ remains in a strong position to meet the housing, business and trading needs of the country,” Ms Watson said.

[1] ANZ New Zealand represents all of ANZ’s operations in New Zealand (NZ Geography), including ANZ Bank New Zealand Limited, its parent company ANZ Holdings (New Zealand) Limited, the New Zealand branch of Australia and New Zealand Banking Group Limited and other New Zealand non-banking entities owned by ANZ.

[2] Statutory profit has been adjusted to exclude non-core items to arrive at cash profit, the result for the ongoing business activities of ANZ New Zealand. Refer to Summary of key financial information for details of reconciling items between cash profit and statutory profit.

[3] BS11 is The Reserve Bank of New Zealand’s new Outsourcing Policy.

[4] KPMG Financial Institutions Performance Survey: Banks – Review of 2022

For media enquiries contact: Briar McCormack, Head of External Communications, +64 21 2801173

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Business

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Community

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

New Zealand

NZ Media Releases

NZ Media Releases

New Zealand

New Zealand

NZ Consumer

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

Media

NZ Consumer

Media

Media

Media

NZ Media Releases

Media

Media

NZ Media Releases

Media

NZ Community