NZ Media Releases

Nagaja Sanatkumar to be appointed to the ANZ New Zealand Board

Nagaja Sanatkumar to join the ANZ NZ Board

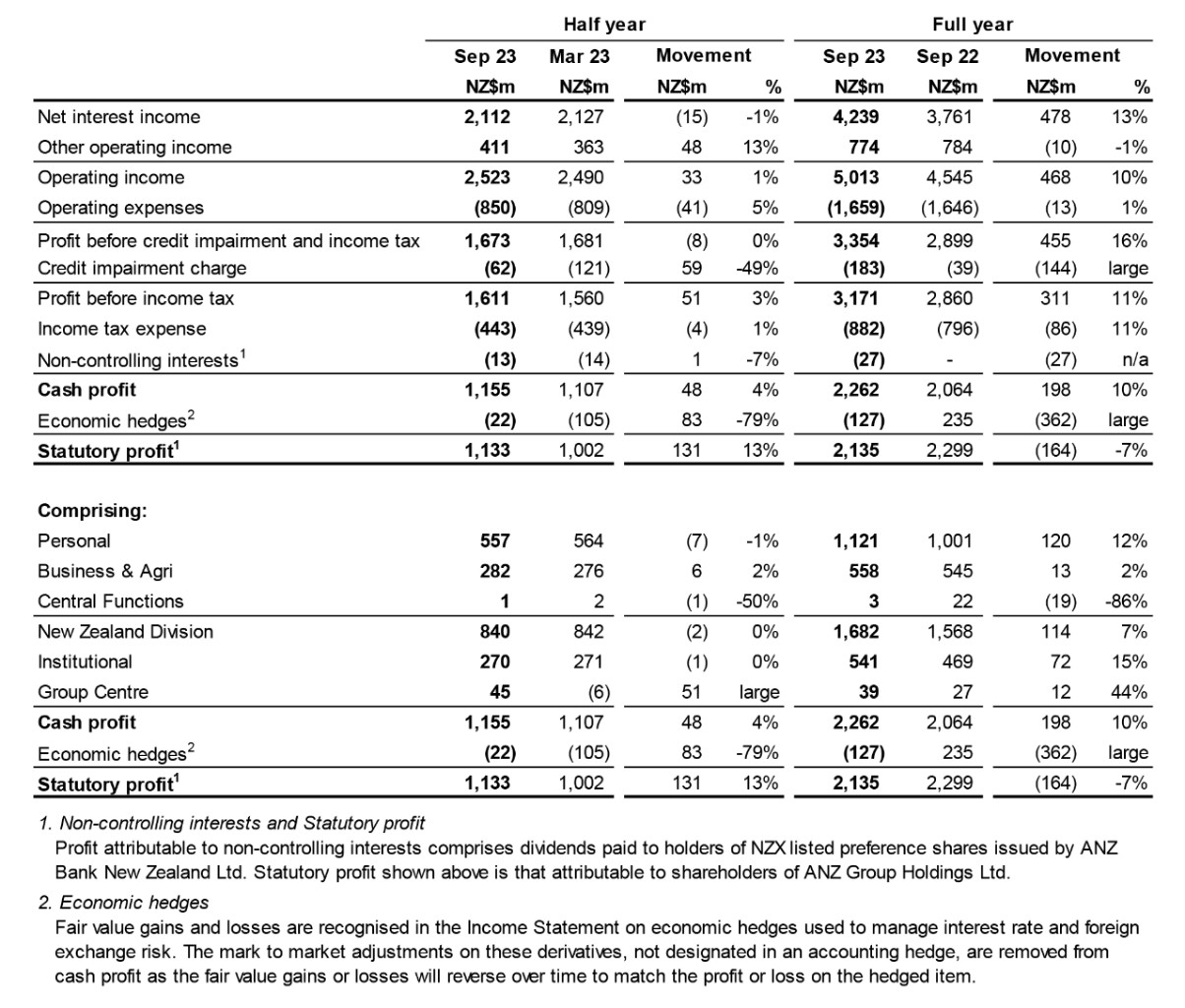

ANZ New Zealand[1] (ANZ NZ) today reported a cash[2] net profit after tax (NPAT) of $2,262m for the 12 months to 30 September 2023, an increase of 10% on the prior year. Statutory NPAT, which includes gains and losses from economic hedges, was $2,135m, down 7%.

ANZ Bank New Zealand Ltd (ANZ Bank NZ) Chief Executive Officer Antonia Watson said this was a good result which positions the bank well for the current difficult economic conditions.

“The year was very much a game of two halves; the good performance of the bank in the first half of the 2022-2023 financial year reflected the tailwinds of the Covid fiscal stimulus in the economy together with a series of rapid increases in the official cash rate.

“But in the second half of the year our performance slowed due to the more difficult environment New Zealand is entering.

However, we’re a well-managed, resilient business and remain well placed to support our customers and the New Zealand economy as we enter more challenging periods,” Ms Watson said.

Revenue for the year was $5,013 million, remaining broadly flat in the second half. Expenses for the year were up $13 million, an increase of 1%, driven by inflationary pressures on staff and vendor costs, offset by lower project spend due to the completion of project work on the RBNZ’s new Outsourcing Policy (BS11).

Market share picked up in the second half and home lending was up 3% for the year despite the difficult conditions. Business and agri lending, however, was down 2% due to a combination of lower commercial property lending and customers remaining cautious about taking on further debt while inflation and interest rates are high. Customer deposits were up 2%.

Continued lending margin compression and deposit mix changes meant the Net Interest Margin – the difference between what the bank borrows money at and what it then lends it out at – for the New Zealand division dropped by seven basis points in the second half of the year.

“That’s because the slower housing market meant banks were fighting even harder for customers, global inflationary pressures saw wholesale interest rates rise and many New Zealanders moved their savings from on call accounts to higher interest earning term deposits.”

She said the bank was prepared for a potentially difficult year ahead, with the new Government facing a number of fiscal challenges and central banks around the world still trying to tame inflation.

“New Zealand is probably headed into tougher times. Inflation is expected to remain above the Reserve Bank’s target range, interest rates will likely be higher for longer and unemployment is expected to rise.”

She said the bank expected to see more stress amongst businesses and mortgage holders.

“The majority of our home loan customers have moved onto higher interest rates, and most have adapted well. A third of home loan accounts are ahead by six months or more. But around 34 percent are on rates lower than five percent with around a third of those rolling onto higher rates over the next six months.”

The bank was closely monitoring how customers were managing and was seeing an increase in the number of people falling behind on payments by 90 days or more.

As a result, she said, ANZ NZ had increased the amount put aside for potential bad debts by $144 million, increasing the total credit impairment provisions to $857 million. The bank is also putting more resources into the customer hardship team in preparation.

In the past 12 months the bank reached out to over 290,000 customers identified as most at risk of financial stress to offer reassurance and support.

She said ANZ NZ had worked hard to support customers as interest rates and cost-of-living pressures continued to rise.

“Strong, well-capitalised banks act as a shock absorber through challenging economic conditions. This means we’re still well positioned to meet the housing, business and trading needs of the country.”

All comparisons are against the prior comparable period and on a cash basis unless noted otherwise

ANZ NZ continued to support Kiwis with their home ownership goals and navigate the rising interest rate environment providing $19.3 billion in new home lending across the year.

“One of the ways we did that was through a campaign giving our mortgage holders reassurance and support when making decisions about home lending. We also offered free, no obligation home loan check-in conversations.”

More than 12,000 people have completed a home loan check-in with many taking follow-up action to manage their financial situation.

The bank also contacted more than 30,000 customers due to refix their home loan at a higher rate to ensure they were aware of the options available to them.

“Our message to anyone feeling financial pressure is to get in touch with us earlier rather than later. Working with your bank gives you time and options; we’re here to help people manage their repayments with targeted support.”

Higher interest rates had benefited savers with term-deposit rates being around five times higher for popular terms than they were before rates began rising. Customer data showed around a quarter of customers were regularly contributing into a savings account and over half had a savings buffer in place.

Business and consumer confidence remained subdued throughout the year.

Non-housing lending to Business & Agri and Institutional customers was down 2 percent, decreasing by $850 million.

“New Zealand businesses have proved resilient and able to adapt to the many challenges they’ve faced in recent years.

“Our team have worked hard to connect and understand what our customers are dealing with and how we can best support them.”

Earlier this year ANZ NZ launched the low-interest Business Regrowth Loan allocating an initial fund of $250 million to support customers and regional economies impacted by significant weather events.

During the year business customers invested more than $30 million in assets or projects that demonstrated environmental benefits through the new ANZ Business Green Loan.

ANZ NZ continued to invest in customer protection, technology, and awareness campaigns to help protect customers from scams and fraud.

“Scams have become a major global issue and better protecting New Zealanders requires coordinated effort between banks, telcos, retailers, social media companies, Government, Police, and regulators,” Ms Watson said.

Two-factor authentication technology helped protect customers from around $6 million in fraud and scams in the past 12 months. In the four months since launch ANZ Fraud Check, a new tool which alerts customers to any card transactions identified as unusual via text message, notified over 150,000 customers instantly when a suspicious transaction appeared on their card.

The bank ran numerous scam education workshops, sent millions of customer fraud education emails, and implemented messaging within goMoney and Internet banking reminding customers to be wary when making payments.

“We’ll continue to work closely with the industry and other relevant parties on a range of measures industry can use to help combat scams and the organised criminal groups responsible.”

During the financial year ANZ NZ was the country’s biggest corporate taxpayer, paying $830 million, employed around 8,000 New Zealanders, paid $560 million to contractors and suppliers, and paid dividends from ANZ Group to New Zealanders, either directly or through KiwiSaver, pension, and managed funds.

This is in addition to the $13 million in contributions to local sponsorships and donations to sports, arts, cultural and community events and $3 million pledged to support Cyclone Gabrielle recovery.

ANZ NZ welcomed the Commerce Commission’s market study into personal banking services.

“With cost-of-living pressures impacting many households, it is important people have confidence in the banking sector.

“We’ve provided evidence that ANZ NZ’s profitability is at a level that is consistent with a competitive banking market and in line with comparable international peers.

“New Zealanders should have confidence in their banks, we’re in a strong position to provide not just assistance for customers, but stability for the economy,” Ms Watson said.

[1] ANZ New Zealand represents all of ANZ’s operations in New Zealand (NZ Geography), including ANZ Bank New Zealand Limited, its parent company ANZ Holdings (New Zealand) Limited and the New Zealand branch of ANZ Banking Group Limited.

[2] Statutory profit has been adjusted to exclude non-core items to arrive at cash profit, the result for the ongoing business activities of ANZ New Zealand. Refer to Summary of key financial information for details of reconciling items between cash profit and statutory profit.

For media enquiries contact:

Kristy Martin, Communications Manager, External Communications +64 21 531402

Briar McCormack, Head of External Communications +64 21 2801173

Approved for distribution by ANZ’s Continuous Disclosure Committee.

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Business

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Community

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Media Releases

New Zealand

NZ Media Releases

NZ Media Releases

New Zealand

New Zealand

NZ Consumer

NZ Media Releases

NZ Consumer

NZ Media Releases

NZ Media Releases

Media

NZ Consumer

Media

Media

Media

NZ Media Releases

Media

Media

NZ Media Releases

Media

NZ Community