NZ Business

The sustainable edge of New Zealand farmers

Businesses that have a focus on emissions stand to improve their productivity and profitability writes ANZ New Zealand Business & Agri Managing Director Lorraine Mapu.

The risks around those doing the borrowing impacts the interest they pay.

Banking is fundamentally about managing risk. In order to lend money to our customers, we rely on funding. This funding comes from shareholders, deposits, or wholesale markets.

Banks manage the risks around their funding by having multiple sources of funding and different timeframes to pay them back. Banks must also manage the risks around who they lend to, what they charge, and for how long.

Like other lending products, agricultural lending interest rates are influenced by factors including economic conditions, regulatory settings, and monetary policy.

Since June 2021 wholesale market interest rates have increased materially and this has resulted in higher lending and deposit interest rates being passed on to customers. The Official Cash Rate has increased from a low of 0.25% in October 2021 to the current rate of 5.50%.

Most New Zealand borrowers will by now have felt some pain from the higher interest rate environment. Farmers are no different.

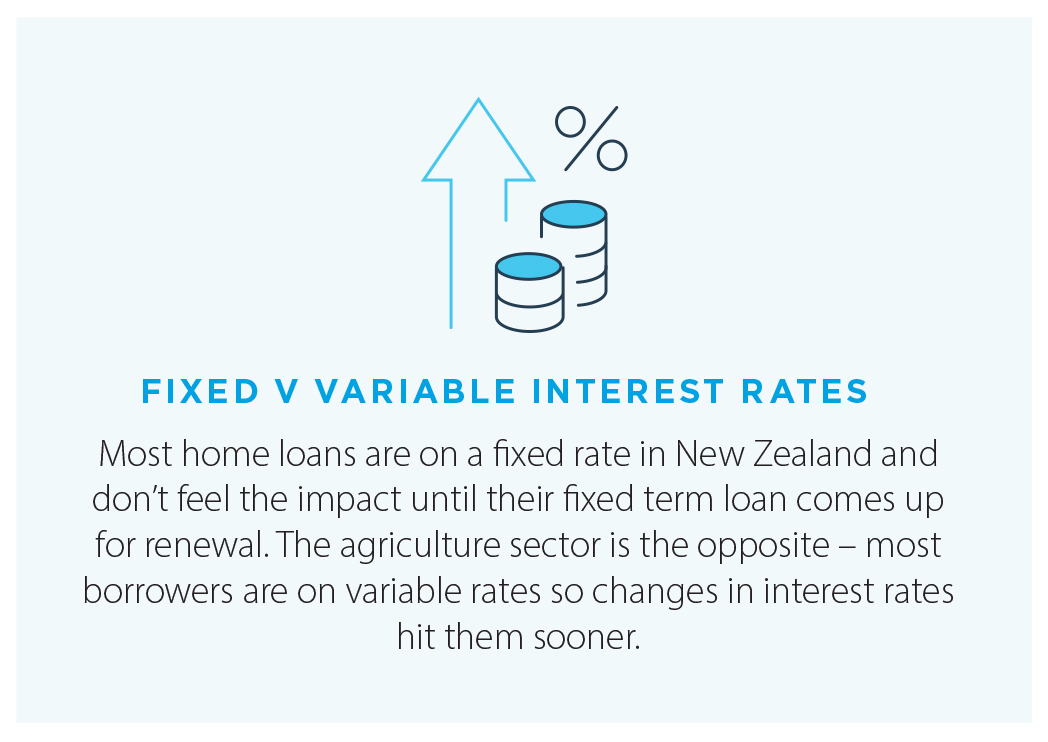

However, agricultural borrowers are likely to have felt that pain sooner than others, due to the nature of their borrowing and the volatile impact of the current economic environment on their costs and markets.

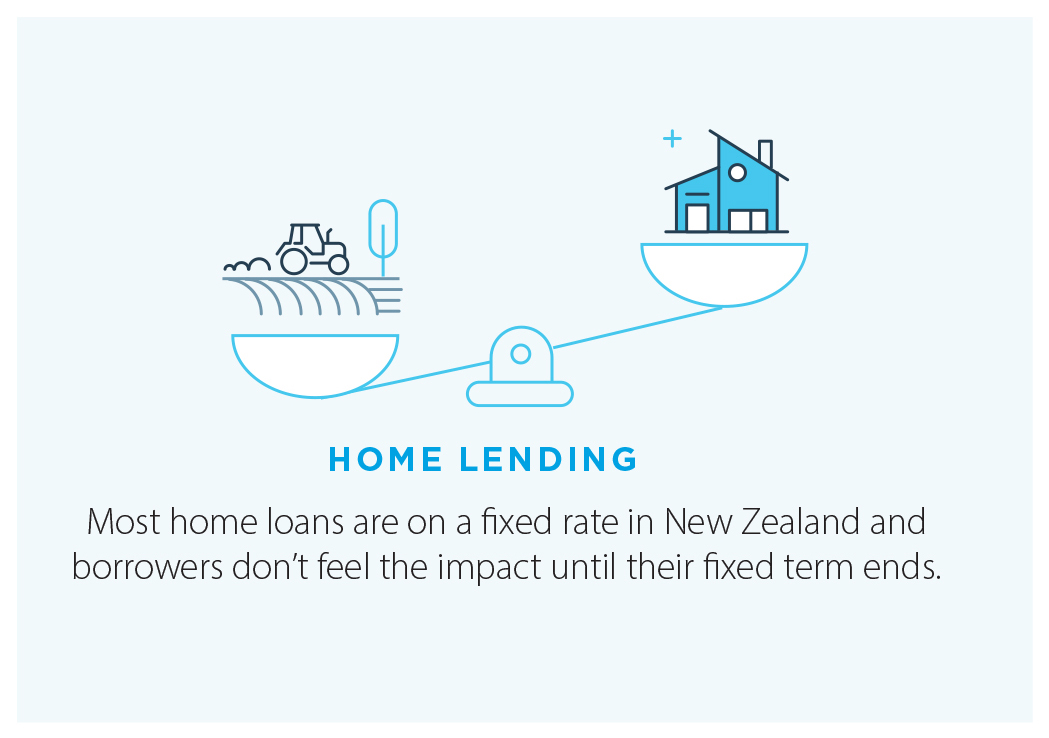

Most home loans are on a fixed rate in New Zealand and don’t feel the impact until their fixed term loan comes up for renewal. The agriculture sector is the opposite – most borrowers are on variable rates so rises in interest rates hit them sooner.

Housing has historically been a stable market. It is well secured, with customers having more certainty of their income to service their lending. The nature of the agriculture sector, on the other hand, means lending is generally considered riskier.

Agriculture is a high profile and important sector; we recognise the critical role the sector plays in supporting the New Zealand economy. A sustainable agriculture sector is vital to our economic well-being.

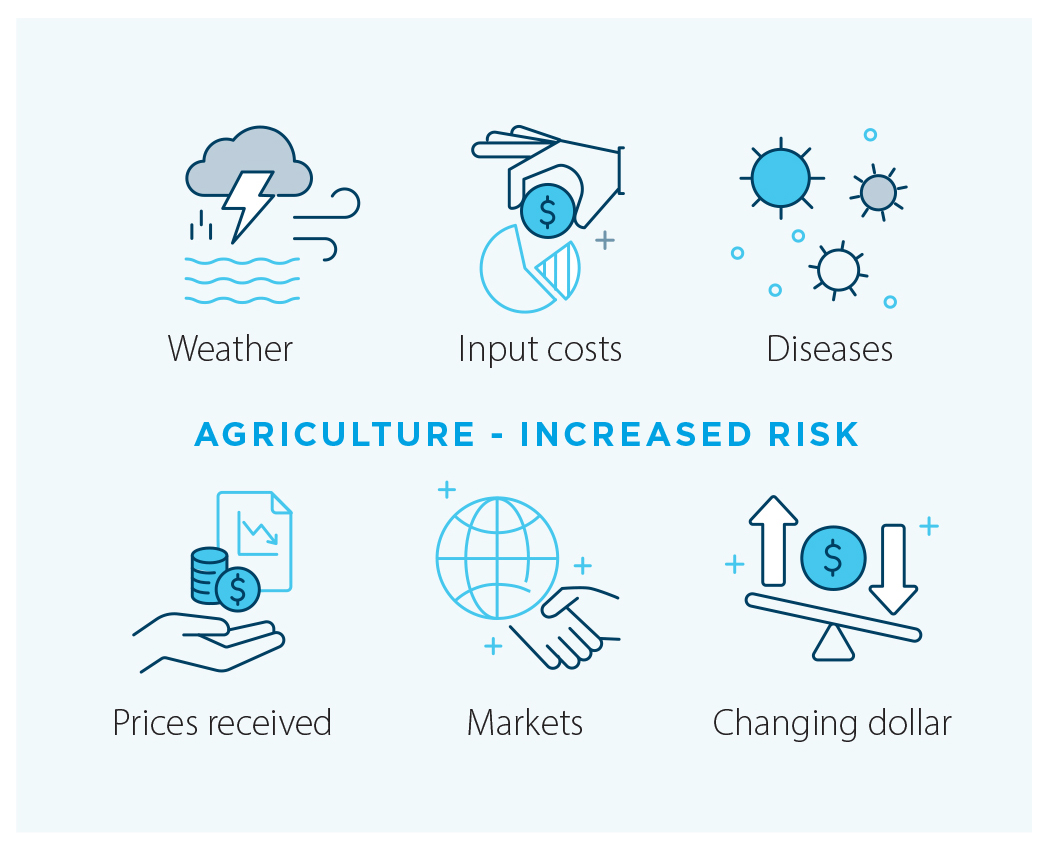

But history shows its performance can fluctuate because it is highly competitive and is impacted by many factors outside the sector’s control such as the weather, input costs, access to markets, diseases, a changeable dollar, and commodity prices.

These factors are reflected in the amount of capital banks must hold against their lending.

Our main regulator, the Reserve Bank of New Zealand (RBNZ), provides us with a capital framework that sets out how much capital we must hold.

It determines how much capital a bank needs to hold based on the risk associated with the lending they have provided their customers. The higher risk a bank’s loans are the more capital it must hold.

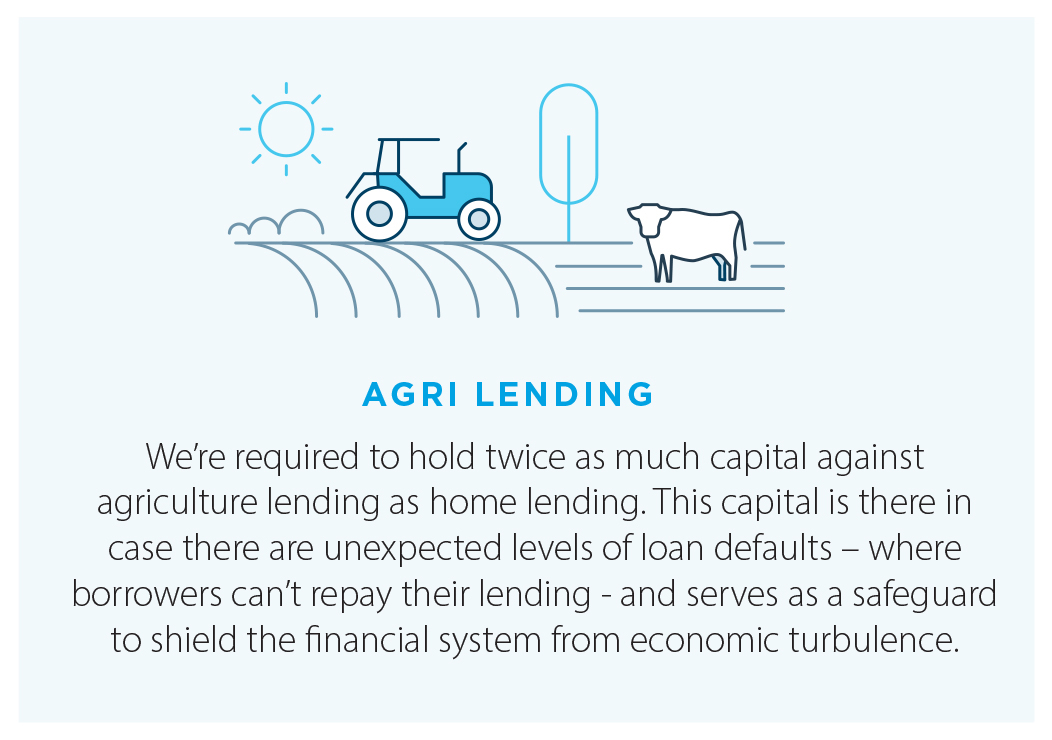

This means we’re required to hold twice as much capital against agriculture lending as home lending.

This capital is there in case there are unexpected levels of loan defaults – where borrowers can’t repay their lending - and serves as a safeguard to shield the financial system from economic turbulence.

The RBNZ did a review of capital requirements in 2019, as other regulators globally have, and banks contributed to that process. Out of this, there have been changes to the RBNZ’s capital framework and banks are now required to hold more capital.

The aim is to further increase financial stability and reduce the risk of banks failing.

But money costs money. That extra capital is funded by bank shareholders and comes at a cost, some of which is passed on to customers.

Currently shareholders are required to contribute around $9 of capital on average for every $100 of lending. This will increase to around $12 for every $100 by 2028.

Not unreasonably, bank shareholders expect an appropriate return for the extra capital required for the same loan.

So, when comparing interest rates between the agriculture lending to home lending, it is expected that lending interest rates would be higher for the agriculture sector due to the level of capital and risk.

The lending interest rate charged ensures an appropriate return when considering the capital requirements along with the operating cost to service customers.

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Community

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Consumer

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Media Releases

NZ Business

NZ Community

NZ Business

NZ Business

NZ Media Releases

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Media Releases

NZ Media Releases

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Sustainability

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Consumer

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Insights

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Consumer

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

NZ Community

NZ Business

NZ Business

NZ Business

NZ Business

NZ Business

NZ Media Releases

Media

NZ Media Releases

NZ Business

NZ Business

NZ Business