NZ Insights

What is 'open banking'?

Open banking is all about customer choice. It will be up to you who you share your personal banking information with.

Liz Kendall

Senior Economist

ANZ New Zealand Ltd.

%20auckland%20nz.jpg/_jcr_content/renditions/cq5dam.web.1331.1024.jpeg)

A number of ongoing themes will shape the way forward in the year ahead.

The COVID-19 pandemic continues to run rampant globally, and our national fortunes will remain crucially tied to our continued success in keeping the virus out.

The path to inoculation will take time, and bumps are possible along the way. Domestically, housing is likely to remain high-profile, with the market ending the year on an unsustainable footing.

A degree of cooling seems likely, and credit conditions may become less permissive, though it is also possible that unaffordability continues to worsen, exacerbating longer-term risks.

Meanwhile, new challenges look set to come to the fore, like the impact of our lost summer of tourism. Businesses have been remarkably resilient, setting us up well to weather this test.

But even so, we need to brace for some impact. Inflation risks have increased too, especially with supply disruptions an ongoing problem, and volatility may return as markets digest the unfolding outlook.

For policymakers, trade-offs are becoming trickier to manage and longer-term issues will rear their heads, along with questions about when policy settings might return to “normal”.

And of course, we will be faced with unknown unknowns in the time ahead – those inevitable uncertainties that will shape the path forward, for better or worse.

2020 was a year for the history books. The world was ravaged by the COVID-19 crisis, policymakers pulled out unprecedented policy tools to combat the fallout, and households and firms faced new and enormous challenges.

Although there are reasons to be optimistic about the future, many of those same challenges are still with us as we enter 2021. Around the world, the massive human and economic toll of the pandemic continues.

Against that backdrop, a number of themes look set to shape the path ahead – some a legacy from 2020, while other new challenges will come to the fore.

As we enter the New Year, a path to eventual normality is now in front of us, with several vaccines for COVID-19 now being rolled out globally.

Eventually, we should be able to achieve widespread immunisation, the world will be able to return to economic normality, and international travel will resume.

But until then, the stakes remain huge – and it isn’t expected to be quick or smooth sailing. Mass inoculation, herd immunity, and border opening on a global scale will take time.

That means that although the development of vaccines represents a turning point in the crisis, the pandemic still casts a long and worrying shadow over the outlook – and risks remain abundant.

Treatment of COVID-19 has improved, but some strains of the virus are now spreading faster than ever. Health systems and economies are under significant pressure, cushioned by an unprecedented policy response.

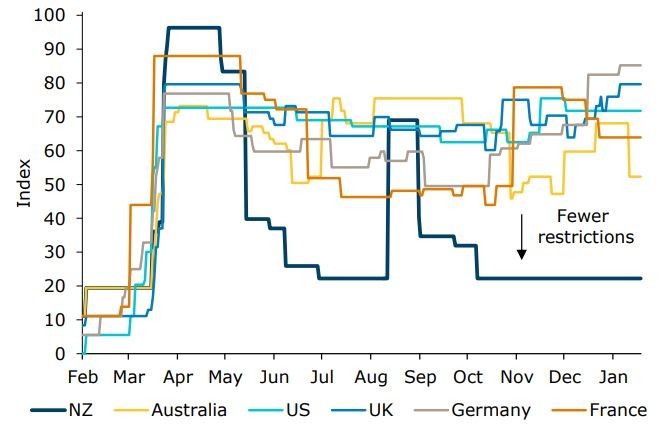

Globally, New Zealand is an outperformer economically, reflecting the success of our health response, which has enabled us to live in relative freedom apart from the closed border (figure 1).

Meanwhile, strict and widespread lockdowns are commonplace in many other countries, and the virus remains an ever-present threat. Truth be told, we don’t know how lucky we are.

Figure 1. Oxford Government Response Stringency Index.

Source: Oxford University.

We expect that widespread inoculation in New Zealand will occur over the second half of 2021, with eventual border reopening from early 2022 – the ultimate game changer for the economic outlook.

The possibility of regional travel bubbles in the meantime could alter economic forecasts, but mostly at the edges, and challenges to establishing these remain high. There may be bumps along the way too.

Until inoculation occurs, the battle will continue here to keep the virus out. Our safeguards have improved and we are better at responding when an outbreak occurs.

But COVID-19 has evolved to become more easily transmissible, meaning tougher restrictions are now required to achieve the same result.

A significant incursion could therefore change our fortunes dramatically and will remain a significant risk until we achieve high rates of immunisation in New Zealand.

Meanwhile, we are still a small trading nation, with our national income susceptible to fluctuations in global demand. Our export prices have held up remarkably well (a trend that has continued into 2021, with dairy prices marching even higher).

Long may that continue. But we do remain vulnerable to the economic fallout globally, even from within our well-locked fortress. The world’s ability to pay a premium for our high-quality exports is being compromised.

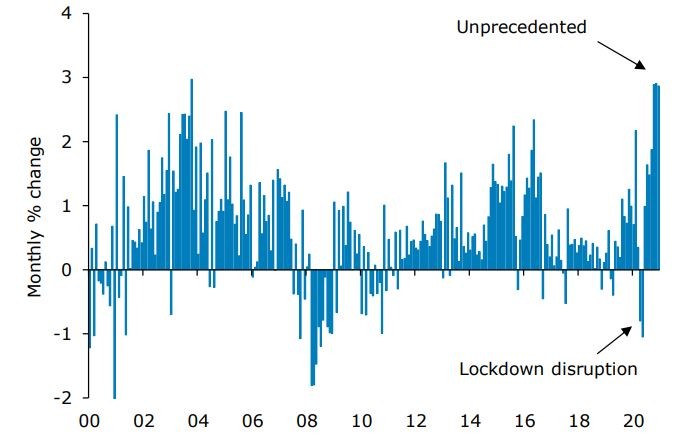

Strength in the housing market through the second half of 2020 was unprecedented, with prices rising 16% since May (figure 2). Increases like that are unsustainable in the context of incomes that have been stable at best.

Figure 2. Monthly house price inflation.

Source: REINZ.

Strength in the housing market is supporting wider economic activity and providing an offset to weakness in other areas, such as tourism and international education – but a key question is how much further the current upturn has to run.

The hot housing market has been a high-profile issue, with low interest rates spurring buyers on and a speculative dynamic at play. Reports of rampant house price inflation have inflamed FOMO (“fear of missing out”) in a tight, supply-constrained market.

This has been a perfect storm for house price rises, but eventually this dynamic will run its course, with affordability and credit constraints weighing on the market and a stagnating economic recovery casting a shadow.

This is expected to take some heat out of the market at some point, but when that will occur is highly uncertain. In the meantime, New Zealand’s issues with acute housing unaffordability continue to worsen.

To reverse the tide, big, bold action is needed urgently (See ANZ Property Focus – Unlocking the solution for more details).

The domestic economy has been remarkably resilient, relative to what was expected last year when we were looking down the barrel of the COVID-19 crisis.

That reflects our successful health response, effective policy action (especially the wage subsidy), and a solid bounce-back in domestic demand. An element of this resilience has been a matter of timing though, too.

It may not feel like it for many, but the impact of the closed border on New Zealand’s economy is highly significant – and seasonal.

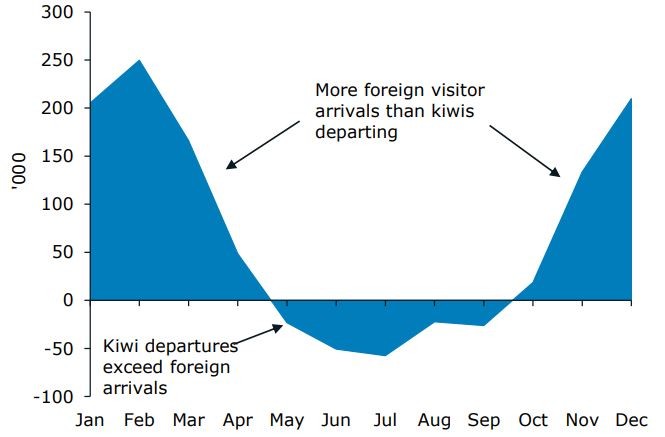

In winter, captive domestic tourists have provided an offset, but that offset is insignificant in the summer months when the influx of international visitors would usually be huge – and kiwis stay home anyway (figure 3).

Some businesses that are exposed to tourism are already struggling, but Q1 is the crunch point, with flow-on effects to other industries, which will see, at best, an economic wobble early in the year.

Figure 3. Typical seasonality of international visitor arrivals.

Source: Statistics NZ, ANZ Research.

The policy outlook for the RBNZ has now moved to a more complicated part of the cycle. The time for big-bang stimulus is over, and it is no longer clear-cut that more stimulus is required.

In November, we outlined a range of possible scenarios for policy depending on economic conditions. See our ANZ Insight for details on these scenarios and our ANZ Property Focus – Bag of tricks for more on how RBNZ policy works, including new unconventional tools.

On balance, a more positive scenario appears to be playing out: the economy is doing better than expected, businesses are resilient, the housing market is running hot, and inflation is no longer a one-way bet.

However, the news is not all positive. A higher exchange rate has seen financial conditions tighten, and mortgage rates have not yet fallen as much as the RBNZ expected.

Meanwhile, the path of unemployment and inflation back to target is not assured, with the RBNZ very conscious of downside risks.

Weighing it up, we have updated our OCR call to just one more cut in May, down 15bp to 0.1%, but we don’t think the RBNZ will feel the need to take the plunge to a negative OCR.

At that point, the RBNZ will deem that it has done enough, then wait and see how developments unfold.

New, challenging questions about policy normalisation will come to the fore – if interest rates aren’t going down, when are they going up?

In our view, the RBNZ will be very keen to provide reassurance that it does not intend to withdraw stimulus any time soon – it will not want to see interest rates move higher.

A continued easing bias is the path of least regrets for the RBNZ for quite some time yet, until the outlook is more assured. That won’t stop markets and commentators asking the question, though.

To push against that speculation, we’d expect to see continued dovishness from the RBNZ, with continued emphasis on downside risks, even in a scenario in which further monetary easing is no longer required.

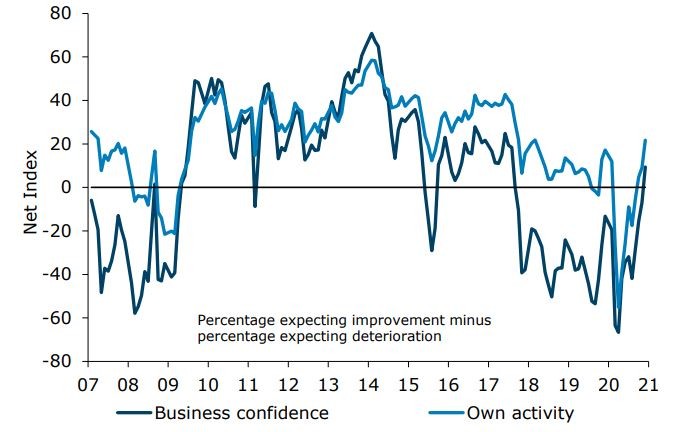

Despite the economy weathering a lockdown-induced sudden stop and the ongoing impact of the closed border, businesses overall are in remarkably good stead according to our ANZ Business Outlook survey.

Indeed, sentiment has continued to push higher in recent months to be above levels seen pre-COVID (figure 4).

Figure 4. ANZ Business Confidence Index and ANZ Own Activity Index.

Source: ANZ Research.

This resilience reflects that incomes were protected and cash-flow pressures were eased during the domestic lockdowns (by way of the wage subsidy, mortgage deferments, and lower interest rates).

Firms did not need to hunker down in response to the downturn, which cushioned the blow and ensured that negativity did not become entrenched. Added to that, domestic demand has bounced back strongly.

The lockdown prohibited households from spending, but the desire was still there.

So when households could go out and spend afterwards, they certainly did – spurred by pentup demand, low interest rates, and an increase in available funds (deferred travel funds and involuntary savings).

Some businesses exposed to the closed border have been really struggling. But in aggregate, income relief and the domestic spending bounce-back has been more than enough to offset this – so far at least.

Of course, this may not remain true going forward, with our lost summer of tourism expected to make conditions more difficult. But with businesses in a better position than had been feared, that gap is now looking easier to offset.

Firms look less vulnerable to a large, sudden change in mood.

If relatively positive sentiment is maintained in the midst of closed border impacts, then that will set the tone for the continuation of a more positive scenario than had been previously expected, and less need for monetary stimulus.

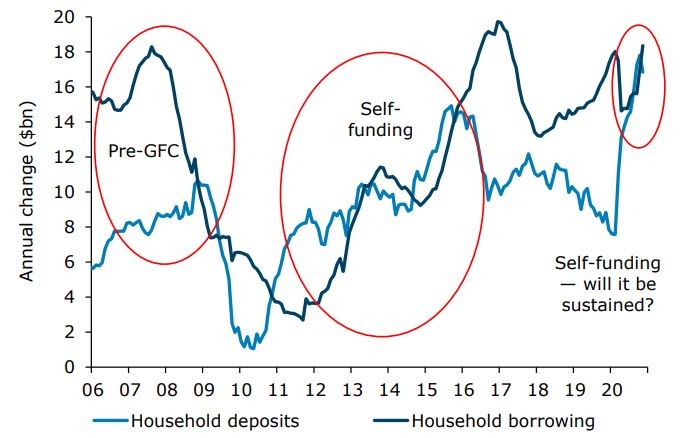

Deposit growth has been very strong this year, since the advent of the RBNZ’s QE programme and the wage subsidy (see our QE FAQs here and here for more details).

This strong deposit growth has helped support lending growth, with abundant funds available to banks to meet very strong demand for mortgages (figure 5).

Figure 5. Bank funding “gap” – household deposits and lending.

Source: RBNZ, ANZ Research.

However, such strong growth in deposits is unlikely to continue.

The ongoing QE programme will continue to support deposit growth, but not to the extent seen last year.

With deposit growth expected to slow to some extent, lending growth is likely to slow too, with banks otherwise needing funds from other sources.

Although other funding options are certainly available (the RBNZ Funding for Lending Programme, for one), banks are likely to be a bit more cautious in an environment where deposit growth is slower, in order to manage their funding needs.

And even if bank funding is plentiful, at some point banks may start to be more cautious about lending terms if the economic outlook is looking more uncertain, or the housing market unsustainable.

A slowdown in lending growth and renewed loan-to-value restrictions are expected to see credit availability reduce to some degree at some stage, resulting in the emergence of a new headwind for the currently buoyant housing market.

On the other hand, strong business confidence and resilient investment intentions may see business credit demand start to improve from very low levels, though likely only very modestly given that the economic recovery is set to stagnate.

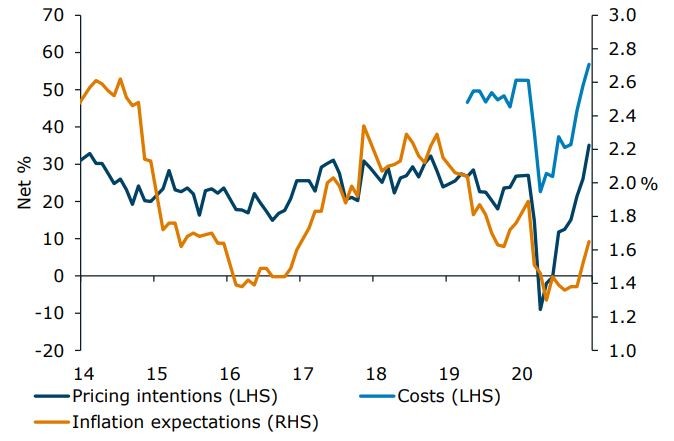

Super-low inflation no longer appears to be a certainty. Cost pressures are starting to emerge, especially as supply disruptions and rising freight costs pinch globally.

And domestically, firms are reporting higher costs and an intention to increase prices, which may see pockets of inflation start to develop.

Typically, “cost-push” inflation is not something to which the RBNZ responds, given that it can be quite short-term in nature and move independently of the overall business cycle.

In fact, cost-driven inflation can be bad for growth and has the potential to weigh on business sentiment if margins are squeezed or price rises impact demand.

But positively, cost pressures are starting to flow through into broader inflation expectations (figure 6). If this is sustained, it could lead to persistently stronger inflation outcomes, even once cost pressures ease.

Up until very recently, inflation expectations have been worryingly low, and the RBNZ has been concerned that this could see actual inflation persistently away from target.

To the extent that inflation expectations rise, this will directly improve outcomes for the RBNZ and reduce the case for more stimulus.

Figure 6. ANZBO inflation indicators.

Source: ANZ Research.

Looking through potential noise on the costs side, the medium-term outlook for inflation has improved too – though there are now risks in both directions.

Inflation expectations are increasing and demand has bounced back strongly, while supply remains a constraint. Even so, headwinds suggest that underlying inflation will face a slow grind higher from here.

The starting point is very low (1.4% y/y), the economic recovery is set to stagnate, and exchange rate increases will partially offset some upward pressure in the short term.

The case for more stimulus from the RBNZ has clearly diminished, but monetary conditions will need to be easy for a long while yet.

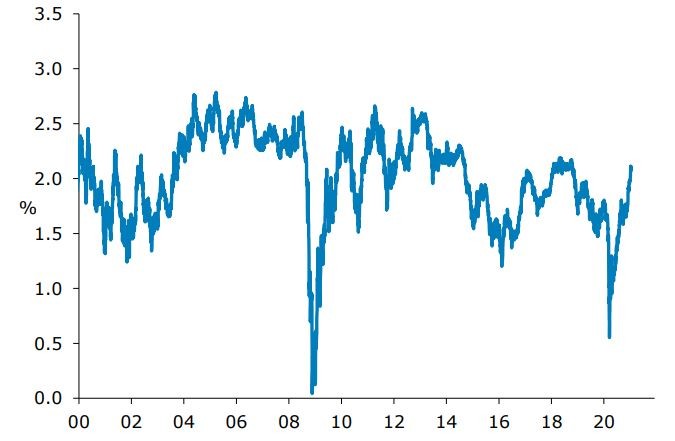

Market pricing for long-term inflation in the US is also trending higher, with cost pressures emerging globally too (figure 7).

Inflation isn’t expected to roar away, particularly given the still-weak demand environment and with the scars of this crisis likely to take some time to heal. But super-low inflation and ever-increasing monetary stimulus is no longer a given.

The economic outlook and the policy response are becoming more nuanced globally.

Market pricing for super-easy policy was a key driver of market developments in 2020 (eg massive increases in equities and very low bond yields). But this view for ever-low interest rates may start to be challenged.

While global central banks will continue to provide reassurance that stimulus will remain in place for a long time, even a small spike higher in bond yields has the potential to spook markets in the current environment.

Figure 7. Market-implied inflation expectations.

Source: Bloomberg, ANZ Research.

Plus, with global economic risks still abundant but not priced, bouts of volatility seem likely.

Markets are grappling with how to weigh up the outlook for eventual normalisation in economic activity – and in time, policy – with the short-term carnage that the pandemic is still wreaking on economies.

This tug of war will continue to set the tone until a clear path out of the woods lies directly ahead.

And at that point, the spectre of tighter monetary conditions globally is likely to loom large, given the massive increase in debt seen in the past year. Even a clear path is likely to be a bumpy one.

Over 2020, fiscal support from the likes of the wage subsidy provided significant support to incomes and activity.

So far, firms have coped very well with the roll-off of these temporary supports, with fewer job losses than previously expected.

But the impulse from the strong demand bounce back has now passed and wage subsidy money has been spent.

The next challenge is to forge a self-sustaining recovery in the absence of fiscal support, and while grappling with continued income challenges as a result of the closed border.

Fiscal spending will need to pivot to growth-supportive policies that will support the level of activity, but growth cannot continue to be underwritten by the Government getting out the chequebook – that would require an unsustainable, perpetual increase in spending.

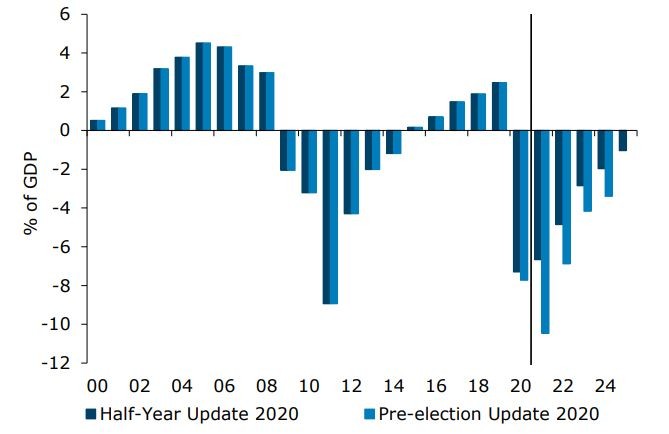

Already, spending (undertaken and planned) is set to see debt levels rise significantly. Borrowing costs are low, but that money doesn’t come from thin air – we do have to pay it back.

Fiscal responsibility requires that the Government rein in its spending deficits over time (figure 8), and this is expected to be a drag on growth in coming years, rather than a boost, at a time when the scars of the economic crisis will still be evident and it may be difficult for the private sector to fill the gap.

We should get more clarity on how the Government intends to get back to “prudent” debt levels early in the year.

We may also see other policy initiatives at the same time, including reform to the RMA, housing initiatives and possible tweaks to migration settings.

Figure 8. Total Crown OBEGAL (Operating balance excluding gains and losses).

Source: The Treasury.

During 2020, the COVID-19 crisis was understandably front and centre and it will dominate the stage in 2021 too. But eventually, as return to normality starts to be in our sights, other longer-term issues will increasingly return to the fore.

Climate change, an ageing population, housing unaffordability and intergenerational equality are all likely to get more attention.

These issues have not gone away, and in some cases the crisis has only seen existing challenges, like housing unaffordability and wealth inequality, worsen.

Policymakers have been focused predominantly on responding to the health crisis that has unfolded before us, but action needs to be taken on these other issues. In some cases, difficult decisions will eventually need to be made.

This time a year ago, most would not have foreseen the global pandemic that was set to hit us, and its enormous impact on the world in 2020.

The themes shaping the outlook changed dramatically as COVID-19 took hold – and the economic outlook shifted many times over the course of the year.

Our understanding of developments was continually tested in new ways, providing a healthy dose of learning. 2020 is now behind us and we can look forward, but challenges clearly remain.

And the pandemic reminds us that while there are many unknowns that we know will shape the path ahead, there are many “unknown unknowns” that could impact our fortunes, for better or worse.

NZ Insights

NZ Business

NZ Insights