NZ Insights

What is 'open banking'?

Open banking is all about customer choice. It will be up to you who you share your personal banking information with.

Miles Workman

Senior Economist

ANZ New Zealand Ltd.

The COVID-19 shock is truly a ‘once in a generation’ event (touch wood). And the macro policy response (ie the response from both the Government and the Reserve Bank) has been appropriately swift and substantial. It has cushioned the blow, even if it is unable to offset and even out the impacts entirely.

But what about the longer-run implications? While necessary, this policy response, in the context of tight housing supply, is leaving in its wake a housing market that is even more difficult to enter for first-home buyers, along with a growing public sector debt burden that will need to be at least partially consolidated through some combination of higher taxes and less government services than otherwise at some point in the future.

Politicians certainly have their work cut out, but they are the only ones who have the tools available to address these issues over the long run. These are structural issues that cyclical policy tools (chiefly monetary policy) are not equipped to address. The trajectory we’re on, as well as New Zealand’s demographic profile, suggests policy makers are going to become more and more attuned to these issues over time as voter concerns evolve.

Although the data is impacted by volatility, the economy has been a lot more resilient to the current crisis than economists initially expected. It remains unclear how much of the positive vibe in the recent data will translate into real, on-theground economic activity in a sustained way, but it’s clear that the monetary and fiscal policy response has been very effective at limiting the initial hit to economic activity.

That’s great news because it means the transition through the recovery (ie once virus risks are contained, and borders reopened) will be a lot easier than otherwise.

The initial macro-policy response has been trying to lean against the turn in the business cycle by limiting the hit to incomes, expenditure and production. For monetary policy, this means making sure credit is flowing smoothly, debt-servicing costs are kept low, and businesses and households have confidence to spend and invest. And the RBNZ has done just that! However, the vigorous response of the housing market has also exposed decades of inadequate policy action from the Government in addressing New Zealand housing supply problems.

For fiscal policy, damage control has meant ensuring that policies limit the income hit, keep people connected to the labour market as far as possible, boost confidence, and stimulate the economy through the recovery – all the while keeping COVID-19 at bay. And to date, the fiscal response has been powerful, essentially paying, through the wage subsidy, for a significant portion of the lost production brought about by lockdowns – at the cost of a lot of government debt.

In addition to the above, fiscal policy has a longer-run role to play by focusing stimulus on bolstering the productive capacity of the economy through investment in key infrastructure and training, addressing regulatory bottlenecks (such as RMA reform), and incentivising businesses to invest. If successful, this part of the policy response could really limit the burden the policy response is currently putting on the younger generation.

Although policy has provided a cushion, that’s not to say there won’t be some permanent scarring brought about by this crisis. A significant amount of damage for some sectors of the economy is unavoidable. Challenges lie ahead, and some colossal forces are pushing and pulling at the economy right now as the lost summer of tourism goes up against strong housing momentum. It’s still not clear where the dust will settle, let alone exactly how virus and vaccine developments will evolve from here, although recent news flow is encouraging.

Unfortunately, we think some of the lost GDP is gone for good – the question is how much. Lockdowns, a closed border, the very sharp and synchronised shock among our trading partners, and the turn in the business cycle more broadly will do that. Here’s how:

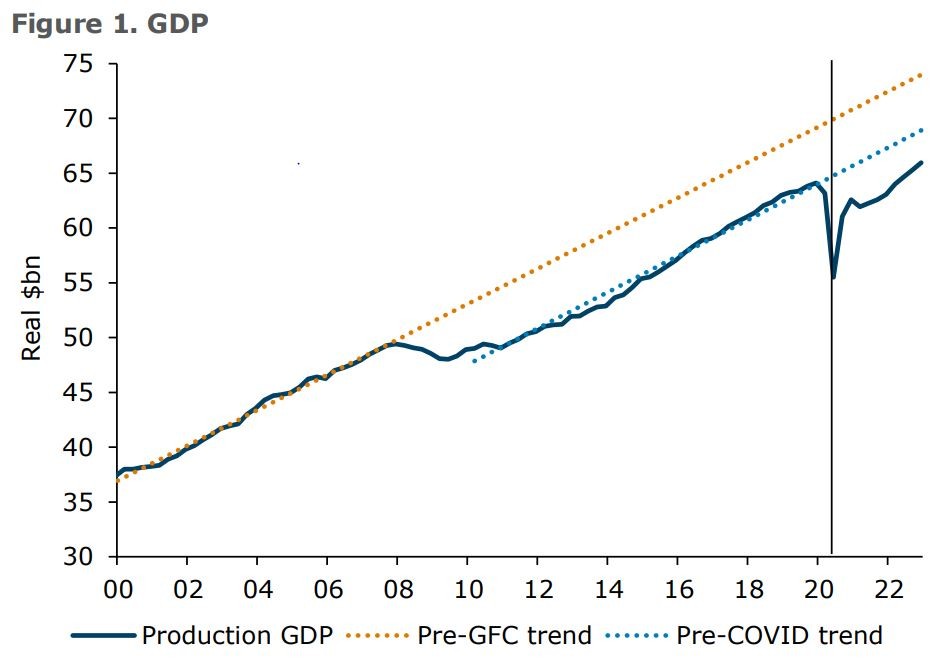

All up, once we’ve navigated the lockdown noise in the data, we expect trend GDP is likely to settle below its pre-COVID trajectory, just as it did following the Global Financial Crisis (figure 1), with it taking even longer for the labour market to return to normal.

Source: Stats NZ, ANZ Research

The swift and significant macro-policy response has been justified. It has reduced job losses, paved the way for higher-than-otherwise aggregate incomes, and therefore a larger tax base, providing more resource for the current and future governments to tackle issues like homelessness and child poverty.

But there’s no such thing as a free lunch. We will have to bear the costs of the response, and this will be disproportionally borne by younger people. And as we discuss in the next section, things on the intergenerational front were looking pretty unfair already.

Intergenerational inequality is running away on us. There is a wide range of factors contributing to this unfortunate development and all of them suggest things are only going to get worse, unless something is done about it.

Source: Statistics NZ

*NZ super is a ‘pay as you go’ system. In practice it means that taxes on activity and incomes today provide the revenue to make super payments to current retirees. This compares to a ‘save as you go’ system, where a generation saves for its own retirement. The difference between the two matters a lot when generation sizes are different.

Source: Macrobond, ANZ Research

Source: The Treasury (Pre-election Update forecasts)

Politicians are under pressure to address these issues, some more urgently than others. Books have been written on these topics, and unfortunately we don’t have any silver bullets to suggest. But there are certainly some key themes that policy needs to focus on.

For housing, the long-term solution is to build more houses. The simple fact is if New Zealand’s housing supply was more responsive to demand, and more building had taken place in the past, the market would be less susceptible to these bouts of rapid house price inflation. This is a structural issue, not a cyclical one, and central and local government are the policymakers with the tools to address this, not the Reserve Bank. Government can bolster supply by reducing red tape, freeing up more land for development, encouraging intensification, helping local councils fund required infrastructure, and incentivising investment and training to lift the productive capacity of the construction industry. There are also ways to limit speculative demand, such as tax changes – though price impacts tend to be of the one-off variety. It’s all easier said than done, of course, and not a quick fix. But looking forward, assessing the Government policy response is pretty straightforward. Does it help increase supply more than it adds to demand? If the answer is no, then the policy is not addressing the fundamental issue.

Sustainable income growth will need to be a real focus as part of the longterm housing strategy, but also as a way to limit the costs associated with the eventual fiscal consolidation. Limiting the initial hit to incomes via the wage subsidy means a stronger-than-otherwise starting point, and that’s definitely going to help over the years ahead. But it’s done and dusted now, and the Government needs to pivot to policies that will boost the productive capacity of the economy. New Zealand’s low-wage problem is essentially a low labour productivity problem. Increased spending on infrastructure (including for residential development) is the obvious go-to here – and absolutely needs to happen. But politicians must not overlook private sector incentives when it comes to investing and taking the right kind of risks that will also influence the economy’s productive capacity. Recent changes to depreciation settings should encourage some additional investment, but more encouragement is needed. Addressing capacity issues with productivity-boosting capital investment rather than simply importing cheap labour as a go-to solution would help housing affordability too. A good hard look at immigration settings to ensure they are income-supportive over the long run is warranted.

A broadening of the tax system will happen eventually. The top 2% of income earners are in for a higher tax bill from 1 April 2021, but that’s just a higher rate on the same people already paying tax. Further, the top 2% of income earners are not necessarily the top 2% when it comes to wealth. Broadening the tax system such as via capital gains, wealth or inheritance taxes, are real possibilities over the longer run. Indeed, if income earners end up doing the heavy lifting of fiscal consolidation while houses remains unattainable to them – even to those earning an average wage – then surely it’s just a matter of time before the tax system is changed to make it fairer for them. The political appetite obviously isn’t there right now, but the debate won’t go away.

Increased scrutiny of government spending is likely to become a key part of the fiscal consolidation in the years ahead too. Budget processes focus on allocating additional spending based on priorities. But often the spending that’s already baked into the fiscal outlook doesn’t get the attention it should; not all of it is achieving the desired result or is an efficient use of tax-payer dollars. Feesfree tertiary study is a great example. It’s very expensive and doesn’t seem to have had much impact on enrolments. Yes, it helps younger people, but it’s helping younger people who are more likely to earn an above-average income anyway, thanks to their qualifications. It would be a different story if it led to higher enrolments, perhaps, but interest-free loans are already subsidising higher future income earners.

We urgently need to take a good hard look at superannuation settings to make them fairer. It’s more complicated than just increasing the eligibility age and/or means testing. Different groups tend to experience different life expectancy rates, meaning a higher eligibility age might not be fair in some cases. Also, the incentives to hide wealth in a means-testing environment can make the system complicated and less efficient. And we’re certainly not advocating that old age pensioners who are just getting by as it is should have to tighten their belts even further. But the fact remains that young people are being short changed, and some recipients of NZ Super don’t need it. And the slower we go on reform, the bigger the mess.

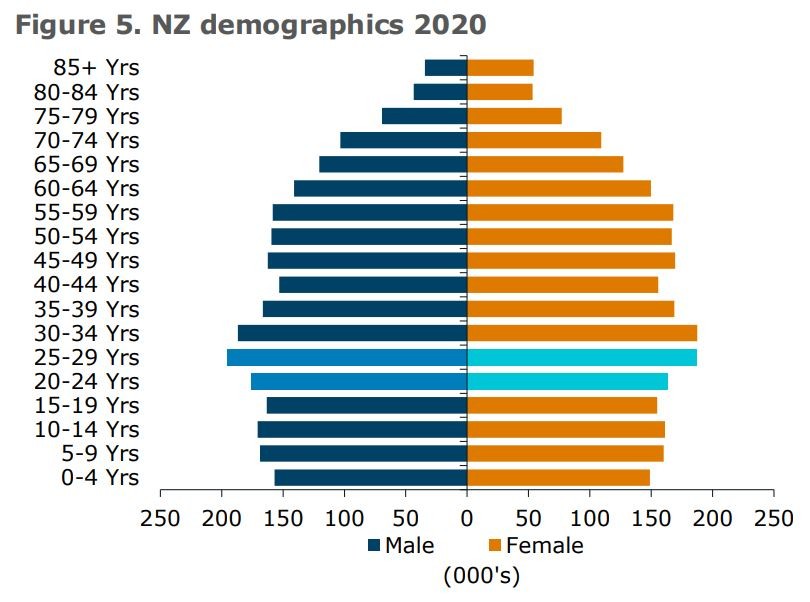

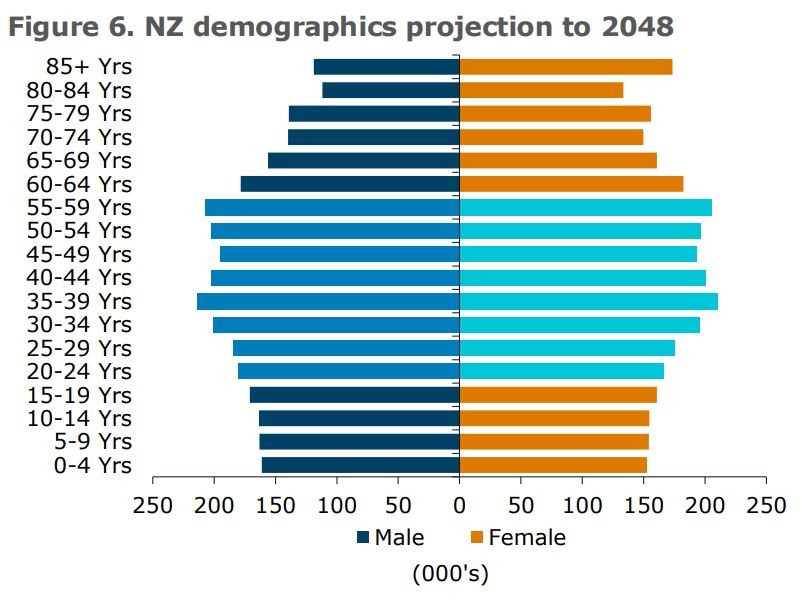

The longer New Zealand stays on its current path, the louder the voices of those adversely affected will get. There’s a significant cohort of 20-29 year olds who currently account for a little less than 20% of the voting population. But fast forward 30 years or so, and this cohort, together with eligible voters younger than them, is projected to account for more than 60% of the voting population (figures 5 and 6). (Stats NZ national population estimates, 50th percentile.)

Source: Statistics NZ, ANZ Research

Source: Statistics NZ, ANZ Research

Of course voter preferences tend to change with age as one’s own financial interests do! By 2050 these 20-29 year olds will be 50-59. This cohort will have (hopefully) paid enough taxes and/or foregone enough government services such that New Zealand’s Government debt position is at a “prudent” level. But will they be close enough to their own retirement that they won’t want to change superannuation eligibility settings too much? Will they own three houses and fight a capital gains tax tooth and nail? One thing’s for sure - over coming years if they don’t, in aggregate, make the steady progression that their forebears did into home ownership and asset accumulation – and that’s looking pretty unlikely at this point – their views on appropriate tax policy are going to be different too. And they’ll vote accordingly, though it may be a slow evolution rather than a wave of radical change.

The fact is, the multi-decade housing boom (ie decades of housing supply failures) has massively enriched the older half of the population at millennials’ expense. Population ageing and a pay-as-you-go system means young people are being asked to support an outsized cohort of non-earners. Millennials are on the hook for the costs of climate change mitigation. And now they’re being hit with the bill for the COVID-19 rescue as well. But in time those same young people will account for the lion’s share of voters and their roar will be heard loud and clear. Politicians beware; 30- and 40-somethings, get saving. Things are going to change – eventually.

NZ Insights

NZ Business

NZ Insights