NZ Insights

What is 'open banking'?

Open banking is all about customer choice. It will be up to you who you share your personal banking information with.

Dean Spicer

Head of Sustainable Finance

ANZ New Zealand Ltd.

Macro global trends in sustainable agricultural are growing in momentum and create an opportunity for New Zealand to take a leadership position in delivering the products that global consumers are demanding. The significance of sustainable practices in farming is only going to become more prominent in the future, and our ability to adapt to these trends will affect the demand and profitability of the sector.

A key aspect of climate change is the importance of water assets to support food production. New Zealand is blessed with natural resources that could provide a significant strategic advantage. How we manage our water resources is fast becoming a key to food security with a need to improve the quality of our waters. If New Zealand is to be seen as a premium brand on the global stage, we need to have a one-nation view to sustainability.

The focus on capital providers to report on their climate related risks is expected to see a shift in capital, redirected to sustainable companies with clear strategies on managing their impacts on the environment and society. Sustainable finance is set to play an important role in transitioning economies to a low carbon basis and promoting social, financial and economic resilience for a future in line with environmental and societal objectives. For those companies that fail to transition, access to capital is likely to become more scarce and expensive. However those that adapt will be rewarded with greater access to capital and increasing demand for their products.

The conscious consumer is driving significant changes in demand for products and services as consumers want to support producers who are ‘doing good’ as well as delivering quality products and services. ‘Doing good’ is often aligned to the sustainability of the product and the associated supply chain. In a research report released by Mindful Money and the Responsible Investment Association Australasia on 29 October, two thirds of those surveyed intend to switch to an ethical KiwiSaver or investment fund. This signals that the conscious consumer is now also a conscious investor.

The global shift in consumer demand and awareness of the importance of sustainability is matched by changes in regulations. The European Union agricultural ministers in October announced a policy change aiming to link farming financial support to the adoption of responsible practices beneficial to the climate and the environment. Another recent significant milestone is the EU Taxonomy passing into EU legislation. This is the establishment of an EU classification system for sustainable practices, and is an important step in freeing up finance for for economic activities that can make a substantial contribution to climate change mitigation or adaptation. Market momentum is partly fuelled by these regulatory changes in Europe, which then feeds into other marketplaces.

Closer to home the New Zealand Government confirmed in September that it will be requiring climate related financial risk reporting for listed corporates and major financial institutions, putting New Zealand on track to become the first country to commit to making this type of reporting mandatory.

The Sustainable Finance Forum (SFF, formed as an initiative of The Aotearoa Circle) released its final report on a roadmap to a sustainable financial system in November. Its interim report highlighted the need for change, where the SFF noted that ‘the global financial system is built on models, norms and rules that do not reflect the full cost of business or respond to changing societal expectations. Integrating environmental and social impacts would improve the accuracy of valuations, accounting and capital adequacy models and internalise social and environmental costs’.

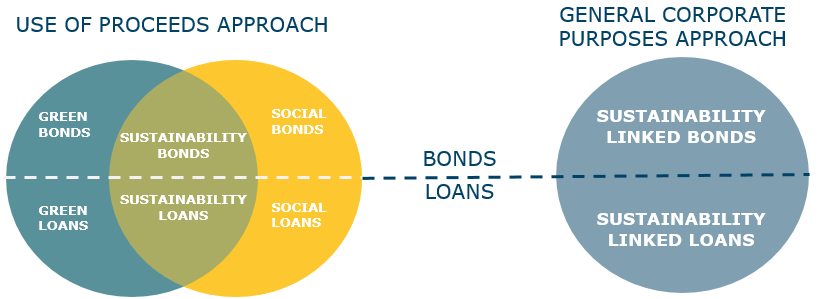

These macro trends have seen a surge in growth and demand for sustainable finance products. There are a number of options for large-scale borrowers to consider. Some of the common sustainable finance products include ‘use of proceeds’ lending such as green loans and bonds, where the finance is attached to an underlying ‘green’ asset.

Other options are general corporate-purpose products such as sustainability linked loans (SLLs) and bonds. With SLLs the interest rate on the loan has the potential to decrease over time if defined sustainability targets are met, in other words, a carrot–and-stick approach with success being rewarded by a cheaper funding rate, or failure requiring the borrower to pay more.

Environmental, social and governance (ESG) considerations are having an increasing impact in the debt capital markets globally – on what investors buy and how borrowers look to raise funds. Sustainable finance products encourage corporate prioritisation of green projects and assets, with many borrowers accelerating an internal push to integrate ESG principles into their business. This internal cultural shift arises as companies become more educated about the green agenda to protect both revenues and reputation.

In the New Zealand context, examples include Mercury NZ Ltd’s financing of the Turitea wind farms and Auckland Council funding Electric Train development. To qualify, the assets need to be certified as meeting one of the evolving global sustainability frameworks, for example the Climate Bond Initiative (CBI) criteria or EU taxonomy. The definition of green assets under these criteria is continually being developed.

Companies that may not have assets that qualify as green may choose to consider a sustainability linked loan. As mentioned above, the financing is linked to predetermined ambitious sustainability targets the lender and the company agree to. If the company meets their targets they receive a funding discount, and should they experience a deterioration they may face an increase in the cost. The structure is intended to align the company’s corporate purpose and sustainability strategy to their financing. Synlait Milk Ltd was the first New Zealand company to complete a sustainable linked loan from ANZ in 2019, with the goal of reducing emissions across a specified time period.

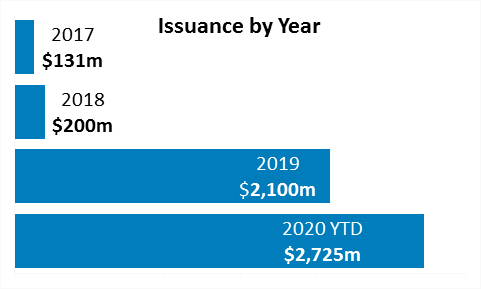

The New Zealand market for sustainable debt products has grown rapidly, with $2,725m in Sustainable bonds issued this year to date. This development is driven by investor demand and companies seeking to connect their sustainability strategy to their funding requirements.

ANZ has lead the development of the market in New Zealand and this year completed a number of market firsts including NZ’s first Inflation Indexed Bond for Housing New Zealand (NZD300m, 15yr), NZ’s largest Corporate Green Bond for Mercury NZ (NZD200m, 7yr), and NZ’s first 30 year Green Bond for Auckland Council which was also the largest Green Bond issued to date in the NZ market (NZD500m, 30yr).

Both Australia and New Zealand require significant investments in green infrastructure and assets to transition to a low carbon economy in line with international commitments. A green-labelled corporate loan market in Australia and New Zealand has emerged in recent years and seen strong growth, with 14 labelled green loans since the first in 2018.

Katharine Tapley, Head of Sustainable Finance at ANZ recently stated that “The market is rapidly moving towards greater awareness and product sophistication, and the new-found interest in green loans is a sign of just how far green financing has come."

Australia and New Zealand Banking Group Limited (ANZ) has pledged to fund and facilitate at least AUD50 billion by 2025 towards sustainable solutions for customers. ANZ also announced new carbon initiatives in October 2020, confirming its commitment to help address climate risk, one of the world’s most pressing sustainability challenges. Activity and targets such as these will boost credit supply for green loans, which along with strong stakeholder and institutional investor demand, could expand the market for green loans.

Qualifying categories for green loans are continuing to evolve, bringing irrigation assets in scope, subject to meeting certain criteria. For example, the installation or upgrade of high efficiency water irrigation system can qualify under the CBI Water Criteria, subject to meeting climate mitigation and adaption criteria.

The climate mitigation component of the CBI Water Criteria is intended to provide transparency over the degree of mitigation that will be delivered over the operational lifetime of the project or asset. Issuers must disclose and justify that their water assets or project do not increase greenhouse gas emissions compared to business-as-usual baseline.

The adaption component of the CBI Water Criteria applies if the asset has an expected or remaining operational lifespan of more than 20 years. In this case an assessment of potential climate risks is required. If these are found to be significant a corresponding adaption plan is required, setting out management responses noting how identified climate risks will be addressed.

Looking ahead, the financing of sustainable business needs to be intrinsically linked to each company’s purpose and its stated sustainability strategy. Investors view green or sustainable debt products the same way any consumer buying a sustainable product would. This means asking does a company have a clear pathway to a carbon neutral future and does it have a social licence to operate?

What is evident is that sustainable financing is here to stay, supported by macro global trends and regulatory requirements. It offers a new and flexible financing source for companies willing to incorporate sustainable principles into their businesses, including operators of irrigation assets. Irrigation operators looking for funding should examine closely whether sustainable finance is suitable for them.

This article was first published by Irrigation New Zealand.

NZ Insights

NZ Business

NZ Insights